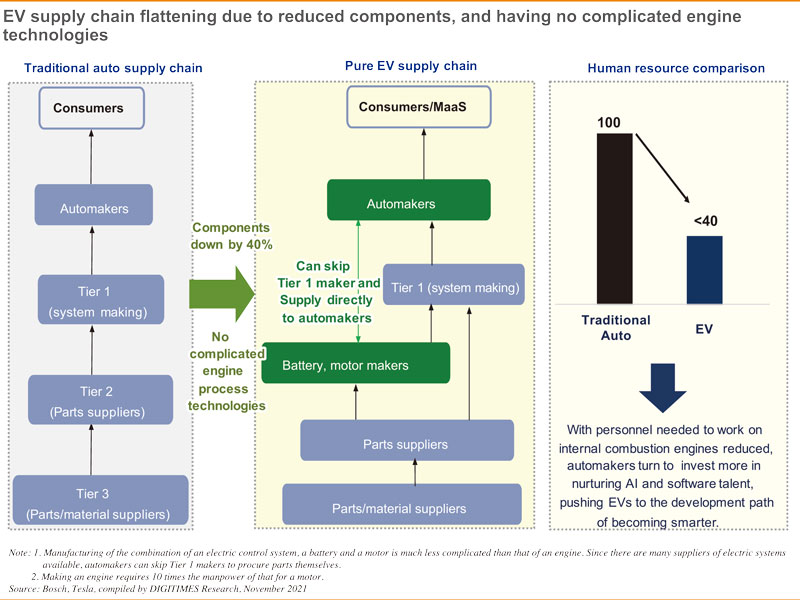

Since EVs are not driven by engines, "design for simplicity" has become a new element to boost EV business opportunities. According to Japan Auto Parts Industries Association, a traditional car has about 30,000 parts, while an EV has only 18,900 parts, which is 37% less. Accounting for 23% of all parts in a traditional vehicle, the engine has the highest complexity. Without the engine, the barriers to car manufacturing are significantly reduced and would encourage many new carmaking forces to get on board. The unchanged parts include the suspension, brakes, and body, while driving, gear shifting, and electronics are the strengths of traditional ICT players. Thanks to a relatively fair and open competitive environment for V2X service providers, new forces are eager to take moves at the initial stage.

Given that EVs have fewer parts and come without complex engine technology, the supply chain would face restructuring and get flatter. What's more, the traditional model of development like making slight changes every three years and introducing a major revamp every five years is bound to change, since the design task is getting less complicated. If the carmaker takes tailor-made orders, it will bypass the traditional hierarchy of operations and go directly to the upstream suppliers.

The shortage of automotive semiconductors in 2021 has accelerated the decomposition of the traditional supply and demand structure. Many carmakers are dealing directly with the original semiconductor vendors to secure more parts. During the process of transition from traditional vehicles to EVs and V2X services, many new fields keep emerging. The evolution patterns and the corresponding business models are both identical to those of ICT industry. Taiwan's IT enterprises that have been well experienced in OEM contract businesses stand a good chance.

It is not too difficult for Taiwan makers to move onward to new markets. Plus, they are building highly complementary partnerships with the new carmaking forces in various countries due to their manufacturing specialties. Engine control units, motors, sensors, panels, etc, are the objects of procurement for major carmakers. Owing to emergence of innovative applications, automakers are now hoping to deal directly with the microLED panel suppliers that used to belong to the Tier 3 to keep updated with the product specifications.

Furthermore, when cars switch from internal combustion engines to EVs, the trend of "smart car" will evolve concurrently. Engineers of the traditional internal combustion engines will be replaced by ones specialize in software and system integration. Various solutions to smart manufacturing will also be widely adopted by the EV supply chain.

In recent years, semiconductor makers have expanded their investments in the V2X service sector. Qualcomm acquired the semiconductor division under the Tier 1 player Veoneer and launched the Chipdragon Ride chip to cash in on the EV business opportunities. The alliance suggests that the market leadership of Tier 1 players is being replaced by semiconductor vendors that integrate SoCs. Nvidia collaborated with the sensor supplier Hyperion 8 and launched its branded SoCs. Most semiconductor players are now keeping an eye on whose chips are to be used in self-driving vehicles on road during 2023~2024. The point is that chip vendors intend to skip Tier 1 players. How would the supply chain become of?