In addition to strong potential video content demand in China, the market has developed rapidly due to government intervention and delays in establishing copyright protections. Content is delivered via traditional broadcasting firms, as well as through the dramatic rise of Internet firms and TV vendors delivering content through connected and smart TVs. There are currently 400 million TVs in use, and each year sales of TVs in China exceed 40 million.

Chart 7: Digital switchover share for cable TV, by provincial-level region, 2011 (%)

Chart 8: Growth in China terrestrial analog and digital TV viewer numbers, 2011-2016 (k households)

Chart 9: China retail color TV 2006-2012 (k units); 2011 market share rankings

Chart 11: Types of online video firm in China and share of advertisement revenues, 1Q12

Chart 12: Size and growth rates for China online video market, 2009-2013 (CNYm)

CMMB is already the world's biggest mobile broadcast TV network

Lack of content and interactivity a bottleneck to CMMB development

Chart 14: User numbers and year-on-year growth rates for IPTV in China, 2006-2012

Chart 19: Changes to IPTV business model before and after tri-network convergence

Chart 20: Strengths and weaknesses of China's video websites

Chart 23: China video website revenue share from advertising, 4Q11

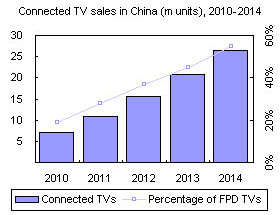

Chart 24: Shipments and penetration rates of connected TVs in China (m units)

Chart 25: Ranking sahre of flat-panel TV sales in China, 2011

Chart 28: Competitions between smart TV and connected TV platforms

Variations in mobile video services among the three main providers

Table 3: Mobile video service strategies among three largest telecom providers

Continuous efforts to increase market share in mobile phone video content

Chart 29: Mobile phone service customers and market share of video content providers