The Taiwan small- to medium-size TFT LCD industry has risen to become the world's largest in terms of LCD cell shipment numbers, while its production value still occupies an important position in the global industry, comparable to that of Japan. Across the strait in China, the nascent small- to medium size TFT LCD panel industry may still be in its development stage, but the country's vast market and strong growth mean the local industry has more potential than that that of any other nation. China-based manufacturers BOE and Tianma have also recently markedly expanded capacity for their respective production of small- to medium size TFT LCD panels and China's competitiveness in the global market is expected to increase dramatically over the next three years.

While players in Greater China market focus on capacity and production for TFT LCD panels, South Korea's Samsung Mobile Display has actively pursued both R&D and manufacturing processes for AMOLED, with this new display technology already posing a significant threat to the high-end small- to medium size TFT LCD sector. Japan's Sharp also plans to switch its 8.5G TFT LCD factory to the production of small- to medium size panels, while Sony Mobile Display, Toshiba Mobile Display and Hitachi Displays are not only set to merge, but are also setting their sights on AMOLED technology and applications. These firms are therefore also likely to present a major threat to small- to medium size TFT LCD manufacturers in the Greater China region. How manufacturers in the Greater China region respond to future competition from Japan and Korea, as well how they go about closing the gap between themselves and Japanese and Korean manufacturers, are topics worthy of careful investigation.

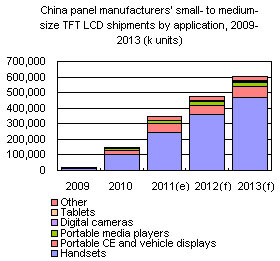

Overview of the small- to medium-size TFT LCD industry in China

Overview of the small- to medium-size TFT LCD industry in Taiwan

Chart 2: Development of Taiwan's small- to medium-size TFT LCD industry

Chart 4: Taiwan shipments of mobile handset panels by supply chain (k units)

Chart 5: Taiwan shipments of vehicle displays by supply chain, 2010-2013 (k units)

Chart 6: Taiwan shipments by application, 2009-2013 (k units)

Prospects for small- to medium-size TFT LCD demand in the Greater China region

Chart 8: Development of the global supply chain for handset TFT LCD panels

Chart 9: Handset panel demand for international and China-based makers, 2010-2011

Chart 10: Greater China makers' handset panel shipments, 1Q10-4Q11 (k units)

Chart 11: Global handset panel shipments by supply chain, 2010-2011

Chart 13: Global demand for nine-inch and larger panels for tablets, 2011

Chart 14: Global demand for sub nine-inch panels for tablets, 2011

Chart 15: Recent trends in the global market for TFT LCD panels for digital cameras

Chart 16: Global shipments of digital still/video camera panels by supply chain, 2010-2011

Chart 17: Recent trends in the global market for portable media players

Chart 18: Portable media player panel demand for international and China makers, 2010-2011

Chart 19: Global shipments of portable media player panels by supply chain, 2010-2011

Chart 20: Medium TFT LCD panel market by application and recent supply chain trends

Chart 21: Medium TFT LCD panel demand by application, 2010-2011

Chart 22: Medium TFT LCD panel demand by application and supply chain, 2010-2011

Chart 23: Status quo for small- to medium-size TFT LCD development in Greater China

Operations and strategies of players in the Greater China region

Chart 24: CMI's quarterly revenues from small- to medium-size TFT LCD panels, 1Q10-2Q11, (NT$b)

Chart 25: CMI's small- to medium-size TFT LCD revenues, 2009-2011 (NT$b)

Chart 26: AUO quarterly revenues from small- to medium-size TFT LCD panels, 1Q09-2Q11, (NT$b)

Chart 27: AUO's small- to medium-size TFT LCD revenues, 2008-2011 (NT$b)

Chart 28: CPT's quarterly small- to medium-size TFT LCD revenues, 1Q09-2Q11 (NT$b)

Chart 29: CPT's small- to medium-size TFT LCD revenues, 2008-2011 (NT$b)

Chart 30: HannStar's quarterly small- to medium-size TFT LCD revenues, 1Q09-2Q11 (NT$b)

Chart 31: HannStar's small- to medium-size TFT LCD revenues, 2008-2011 (NT$b)

Chart 32: Wintek's quarterly small- to medium-size TFT LCD revenues, 1Q09-2Q11 (NT$b)

Chart 33: Wintek's small- to medium-size TFT LCD revenues, 2008-2011 (NT$b)

Chart 34: Giantplus' quarterly small- to medium-size TFT LCD revenues 1Q09-2Q11 (NT$b)

Chart 35: Giantplus’ small- to medium-size TFT LCD revenues, 2008-2011 (NT$b)

Chart 36: E-Ink Holdings' quarterly small- to medium-size TFT LCD revenues, 1Q09-2Q11

Chart 37: E-Ink Holdings' small- to medium-size TFT LCD revenues, 2009-2011 (NT$b)

Chart 38: BOE's small- to medium-size TFT LCD revenues, 2009-2011 (CNYb)

Chart 39: Tianma's small- to medium-size TFT LCD revenues, 2009-2011 (CNYb)

Chart 40: Essential technologies for small- to medium-size TFT LCD manufacturers to win customers

Development of AMOLEDs by Japan and Korea-based manufacturers

AMOLED development by manufacturers in Japan and South Korea

Chart 44: Samsung Mobile Display's Pentile sub-pixel technology

Table 13: CMI and AMO's existing capacity that could be switched to AMOLED panel production

Table 14: Investment plans for major AMOLED players in China