Looking at the development of the Greater China IC design industry during the period 2006-2010, overall output value rose 60% from US$12.3 billion in 2006 to US$19.7 billion in 2010. Within these figures, output value for the Taiwan industry grew 40% to US$14 billion, while output value for the China industry grew 140% to US$5.7 billion.

Thanks to increasing independent product development capabilities and a corresponding rise in the self-supply rate (i.e. sourcing from within China) of components, Digitimes Research believes that the Greater China IC design industry will continue to exhibit growth performance well above the global average.

However, with the slowdown in PC market growth and the explosion in demand for mobile devices becoming increasingly apparent, Taiwan-based design houses have begun to turn their attention to emerging applications including USB 3.0 and touch ICs. Meanwhile the explosion in demand for mobile devices and TV applications has benefitted local IC players in the China market.

In addition, challenges remain for players throughout the Greater China region. The mobile baseband IC sector, for example, is faced with the challenge of turnkey solutions provided by major international vendors, with the result that design houses are actively engaging in mergers and acquisitions to tackle this threat head on.

China-based firms' progress in chip design technology capabilities should also not be overlooked; a number of design houses have even managed to win a place in the ranks of chip suppliers for tier-one brands, and are no longer merely competing on price and forcing prices down across the industry. China-based firms are now represented across all areas of the mobile communications sector, and this comprehensive presence is projected to become a major driver of growth for the China IC design industry in the future.

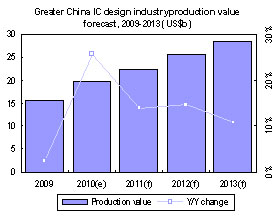

Digitimes Research believes that this strong presence and the increasing chip design technology level in the mobile communications sector will enable the Greater China IC design industry to sustain growth performance seen during the 2006-2010 period, becoming a driving force that will allow the sector to achieve growth well above the global average. Production value for the Greater China IC design industry is projected to reach US$28.4 billion in 2013.

Chart 1: Taiwan share of global shipments in various electronic product segments, 2010

Chart 3: China share of global electronic product shipments, 2010

Chart 5: IC market revenue breakdown by segment, China and Worldwide, 2010

Chart 8: Greater China share of global IC market scale, 2006-2010

Chart 9: IC market revenue breakdown by IC type, China and Worldwide, 2010

Chart 10: Taiwan IC industry production value, 2006-2010 (NT$b)

Chart 11: Taiwan IC industry production value by sector, 2006-2010

Chart 12: China IC industry production value, 2006-2010 (CNYb)

Chart 13: China IC industry production value by sector, 2006-2010

Chart 14: Greater China IC industry production, 2006-2010 (US$b)

Chart 15: Greater China IC industry’s share of global production value, 2006-2010

Table 2: The world's top 10 semiconductor firms, 2010 (US$b)

Chart 16: Global position of the Greater China IC design industry in 2010

Chart 17: Global position of the Greater China foundry industry in 2010

Table 5: Taiwan representatives in Worldwide top 5 SATS firms, 2010 (US$b)

Current developments and trends in the Greater China IC design industry

Chart 18: Total number of Taiwan-based IC design firms, 2000-2009

Chart 19: Taiwan IC deisgn industry production value, 2006-2010 (NT$b)

Table 6: The top 10 Taiwan-based IC design firms in 2010 (NT$b)

Table 7: Market share and rankings for Taiwan's top 10 IC design firms, 2006, 2010

Chart 22: China IC design industry production value, 2006-2010 (CNYb)

Table 9: Market share and rankings for China's top 10 IC design firms, 2006, 2010

Chart 24: Greater China IC design industry production value, 2006-2010 (US$b)

Chart 25: Greater China IC design industry production value as proportion of global total, 2006-2010

Table 10: Rankings for the top 10 IC design firms in the Greater China region, 2010 (US$b)

Table 11: Market share and rankings for top 10 IC design firms in Greater China, 2006-2010

Chart 27: Greater China mobile baseband IC vendor revenues and growth, 2009-2010 (US$b)

Chart 29: Greater China mobile peripheral chip vendor revenues and growth, 2009-2010 (US$b)

Chart 31: Greater China network communcations chip vendor revenues and growth, 2009-2010 (US$b)

Chart 32: Mergers/acquistions involving major global network communcations chip vendors, 2010-2011

Chart 33: Greater China TV controller IC chip vendor revenues and growth, 2009-2010 (US$b)

Chart 34: Greater China LCD driver IC vendor revenues and growth, 2009-2010 (US$b)

Chart 36: Greater China niche DRAM vendor revenues and growth, 2009-2010 (US$b)

Chart 37: Global DRAM bit demand share by application, 2007-2011

Chart 38: Greater China NAND flash controller IC vendor revenues and growth, 2009-2010 (US$b)

Chart 40: Greater China analog IC vendor revenues and growth, 2009-2010 (US$b)

Chart 41: Timeline of Texas Instruments' analog IC production capacity expansion, 2009-2010

Chart 42: Greater China design service and SIP vendor revenues and growth, 2009-2010 (US$b)

Chart 44: Taiwan IC design industry production value forecast, 2009-2013 (NT$b)

Wireless communications chip sector faces a challenge from international firms

Chart 45: Comparison of operations among international mobile chip solution vendors

Emerging applications are inseparable from the development of local industries

Chart 47: China IC design industry production value forecast, 2009-2013 (CNYb)

Chart 48: Products from Tier-1 brands that use chip solutions from China-based IC design houses

Chart 49: China-based IC design houses representation in mobile communications sector products

Chart 50: Greater China IC design industry production value forecast, 2009-2013 (US$b)

Chart 51: Greater China share of global IC design industry production value, 2009-2013

Chart 52: Greater China IC design industry production value share by region, 2009-2013