Figure 1. AI boom timeline

Figure 2. AI technology relationship diagram

Figure 3. Key LLM trends for 2026

Figure 4. M-shaped LLM parameter trend

Figure 5. LLM feature highlights

Figure 6. AI technology trends

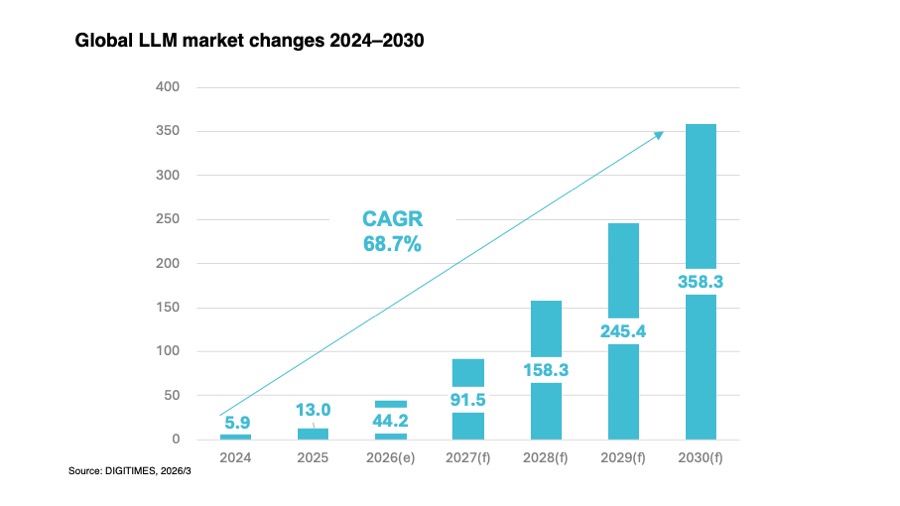

Figure 7. Global LLM market size, 2024–2030

Figure 8. Generative AI market forecast, 2028

Figure 9. Generative AI chatbot hot spots, 2025–2028

Figure 10. Generative AI software development hot spots, 2025–2028

Figure 11. Generative AI image generation hot spots, 2025–2028

Figure 12. Generative AI video generation hot spots, 2025–2028

Figure 13. Enterprise operations automation hot spots, 2025–2028

Figure 14. Process automation hot spots, 2025–2028

Figure 15. Compute deployment factors for generative AI applications

Figure 16. Enterprise AI adoption conditions challenges

Figure 17. Enterprise AI service resources and characteristics

Figure 18. Enterprise AI deployment decision factors

Figure 19. Enterprise AI service supplier landscape

Figure 20. CSP AI service offerings and strategies

Figure 21. Enterprise software vendors' AI strategies

Figure 22. Enterprise IT vendors' AI strategies

Figure 23. AI model startups' enterprise strategies

Figure 24. Supplier positioning and cloud share comparison

Figure 25. Enterprise AI architectures: current and outlook

Figure 26. Supplier advantages and application scenarios

Figure 27. Enterprise AI market drivers and trends

Figure 28. Enterprise AI market outlook

Figure 29. LLM training compute demand forecast

Figure 30. OpenAI o1 model accuracy: training vs inference

Figure 31. Key factors in inference hardware performance

Figure 32. Nvidia Hopper vs Blackwell inference performance

Figure 33. Cloud capex YoY forecast, 2022–2027

Figure 34. AI workload requirements for critical server components

Figure 35. Nvidia traditional vs Dynamo inference

Figure 36. Rubin CPX vs Rubin200 GPU specs

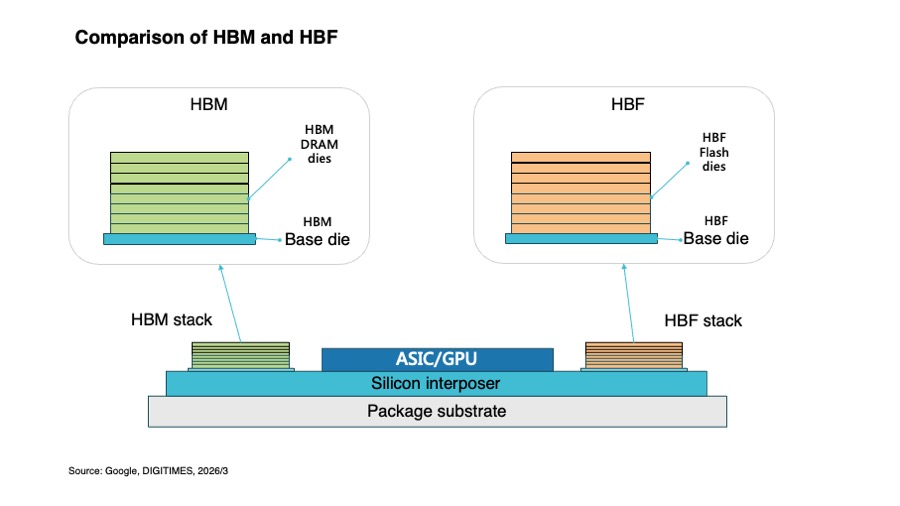

Figure 37. HBM vs HBF packaging comparison

Figure 38. 3D memory-logic stacking architecture

Figure 39. Google AI IaaS evolution

Figure 40. Google AI SaaS evolution

Figure 41. Google accelerator adoption and outlook

Figure 42. Google high-end AI server shipments, 2023–2028

Figure 43. Amazon AI IaaS evolution

Figure 44. Amazon accelerator adoption and outlook

Figure 45. Amazon high-end AI server shipments, 2023–2028

Figure 46. Microsoft AI IaaS evolution

Figure 47. Microsoft AI SaaS evolution

Figure 48. Microsoft AI PaaS evolution

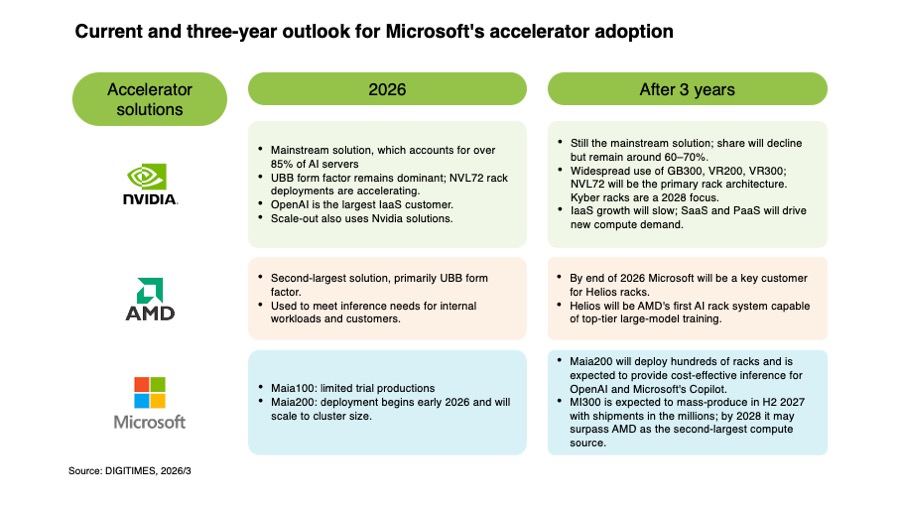

Figure 49. Microsoft accelerator adoption and outlook

Figure 50. Microsoft high-end AI server shipments, 2023–2028

Figure 51. Oracle AI IaaS evolution

Figure 52. Oracle AI PaaS evolution

Figure 53. Oracle AI SaaS evolution

Figure 54. Oracle accelerator adoption and outlook

Figure 55. Oracle high-end AI server shipments, 2023–2028

Figure 56. Traditional vs GEM-model recommender comparison

Figure 57. Meta accelerator adoption and outlook

Figure 58. Meta high-end AI server shipments, 2023–2028

Figure 59. xAI LLM training compute demand forecast

Figure 60. xAI high-end AI server shipments, 2023–2028

Figure 61. ChatGPT vs Claude feature comparison

Figure 62. OpenAI accelerator adoption and outlook

Figure 63. OpenAI high-end AI server shipments, 2023–2028

Figure 64. Anthropic accelerator adoption and outlook

Figure 65. Anthropic high-end AI server shipments, 2023–2028

Figure 66. Global high-end AI server shipments, 2023–2028

Figure 67. Market share by major players, 2023–2028

Figure 68. Market share by accelerator platforms, 2023–2028