Taiwan has been the powerhouse in the TFT LCD industry in the Greater China region. It still is, but China is now also emerging as a big player, bolstering the region's importance in the LCD panel industry. The Greater China region (Taiwan and China) is expected to account for 44.5% of global large-size TFT LCD panel shipments and 42.5% of global large-size capacity in 2011. Geographically speaking, Greater China is the second most important region after South Korea in the panel industry.

The rise of China to becoming a major large-size LCD panel supplier is being facilitated both by its role as the world's factory and by its huge domestic demand. Even though the rising salary levels in Chinese coastal areas have been sending manufacturers looking for cheaper labor in inland regions or other countries, the supply chain in China still boasts high efficiency and cost-effectiveness. In the foreseeable future China will remain the biggest production base for end products using large-size TFT LCD panels. DIGITIMES Research predicts China's share of global production of end products with large-size TFT LCD panels will be able to remain above 73% at least until 2013. Furthermore, demand for end products from the domestic market and exporters will continue to require China to import or locally produce large amounts of TFT LCD panels in the next five years. This will enable China's development into a major large-size LCD panel production base.

The current global economic woes may be slowing down China's progress towards becoming a powerhouse in the large-size TFT LCD panel industry. Its own players are still eager to ramp up capacity, but foreign competitors have all delayed their plans to build advanced panel lines in China. But these foreign players may change their mind next year if China raises tariffs on imports of large-size panels. It remains to be seen how much the tariffs may go up. If the increase is small, these foreign players may find it less pressing to speed up their plant projects. But if the tariffs go up to 8-12% from the present 3-5%, profits for panel exports to China will take a significant blow, forcing them to be more active in building their production facilities in China.

Within the Greater China region Taiwan-based panel makers AUO and CMI will still maintain a 30% share or even more of global large-size TFT LCD shipments by 2013, and their China-based competitors have a good chance of increasing their share to more than 10% by 2013, thanks to domestic demand and the support of the Chinese government's tariffs policy.

The DIGITIMES Special Report "Development trends in the Greater China large-size TFT LCD industry" offers a comprehensive overview of the development of the large-size TFT LCD panel industry in the Greater China region, as well as the competition and collaboration between China-based players and their peers from Taiwan and South Korea.

Development trends of Greater China large-size TFT LCD industry

Chart 1: LCD panels imported to China grew nearly 10 times from 2003-2010( US$b)

Chart 2: Taiwan large-size TFT LCD panel shipments and global share, 4Q10- 4Q11 (k units)

Chart 3: Global large-size TFT LCD panel capacity share by manufacturing region, 2008-2013

Large-size TFT LCD supply-demand trends and impact on suppliers

Chart 5: Global large-size TFT LCD panel demand, 2009-2013 (k square meter)

Chart 6: Large-size TFT LCD panel capacity annual growth by maker, 2009-2013

Chart 7: Global large-size TFT LCD panel capacity, 2008-2013 (k square meter)

Chart 8: Impact of Korea's free trade agreements (FTA) with major economies

Fewer incentives for foreigners to set up LCD panel plants in China?

Chart 9: China LCD monitor production and global market share, 2008-2013(k units)

Chart 10: China notebook production and global market share, 2008-2013 (k units)

Chart 11: China tablet production and global market share, 2010-2013 (k units)

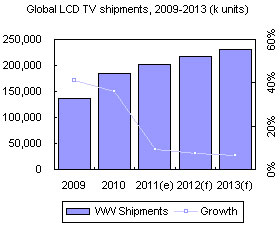

Chart 12: China LCD TV production and global market share, 2008-2013 (k units)

Chart 13: World's largest LCD TV ODM TPV Technology, capacity by geographic region (m units)

Chart 14: China total productionof LCD display systems, 2008-2013 (k units)

Analysis of operations and development strategies of China LCD panel makers

Chart 15: BOE Technology revenue and operating margin, 2006-1H 2011 (CNYm)

Chart 16: BOE revenues and gross margins, by main product line, 2010 (CNYm)

Chart 17: BOE annual changes in gross margins, by main product line, 2009-1H2011

Chart 18: BOE, AUO, CMI, CPT, and LGD's annual changes in operating margin, 2006- 1H2011

Table 1: BOE's TFT LCD production line capacity and applications

Chart 19: BOE 8.5G plant's lead narrowed by CSOT in terms of mass production (substrates/month)

Chart 20: BOE's strategies after mass production of its first 8.5G plant

Chart 21: CSOT 8.5G TFT LCD production line capacity roadmap, 2011-2012 (k substrates/month)

Chart 23: TCL domestic and export LCD TV shipments, 2009-2011 (k units)

Significance of cross-investments between Samsung and TCL Group

Chart 26: China's tariffs on LCD display imports and forecast, 2008-2012

Analysis of operations and development strategies of Taiwan panel makers

Chart 28: AUO remains number four worldwide by overall revenues, 2Q10-2Q11 (NT$m)

Chart 29: AUO revenues and operating profit margins, 2006-2011 (NT$m)

Table 2: Capacity and applications for AUO's TFT LCD factories

Chart 30: CMI revenues and operating profit margins, 2006-2011 (NT$m)

Table 3: Capacity and main applications for CMI's TFT LCD factories

Chart 31: Revenues and operating profit margins for AUO and LGD, 1Q10-2Q11 (US$m)

Chart 33: CPT's revenues and operating margins, 2006-2011 (NT$m)

Table 4: Capacity and main applications for CPT's TFT LCD factories

Chart 34: large-size panels accounting for smaller share of CPT shipments, 2Q10-2Q11