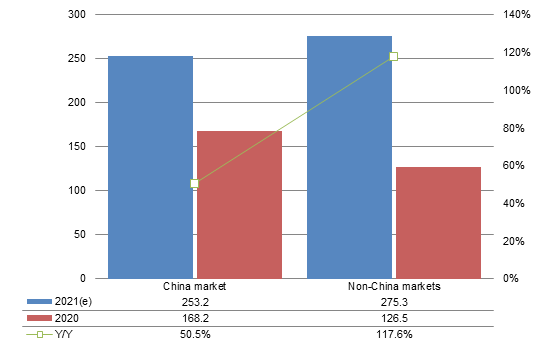

Chart 1: Global smartphone shipments by China and non-China markets, 2020-2021 (m units)

Chart 2: Global smartphone shipments by quarter, 1Q20-4Q21 (m units)

Chart 3: Smartphone shipments in China and non-China markets, 3Q20-4Q21 (m units)

Chart 4: Global shipments by top brands, 2H20, 2H21 (m units)

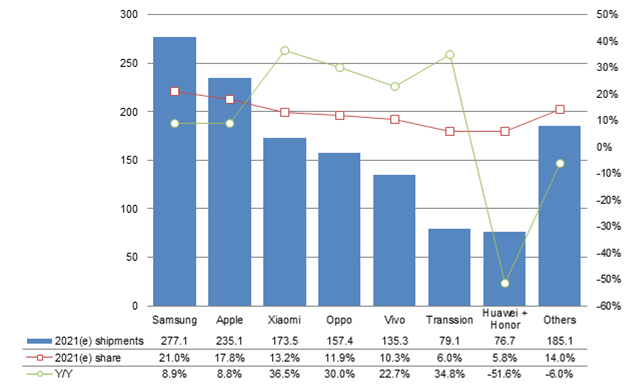

Chart 5: Global shipments and share by top brands, 2021 (m units)

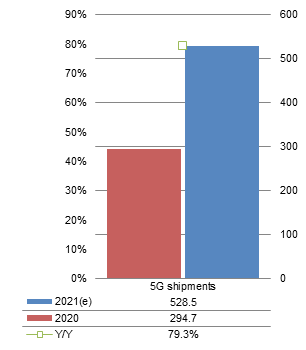

Chart 6: Global 5G smartphone shipments, 2020-2021 (m units)

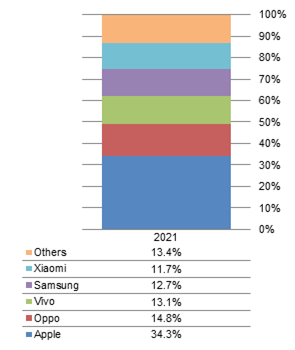

Chart 7: Global 5G smartphone shipment share by top brands, 2021

Chart 8: 5G smartphone shipments in China and non-China markets, 2020-2021 (m units)

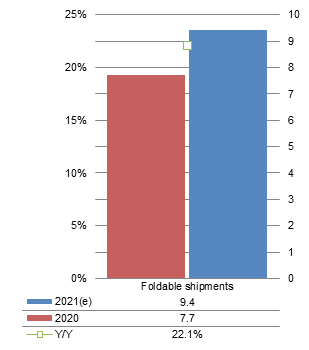

Chart 9: Global Foldable smartphone shipments, 2020-2021 (m units)

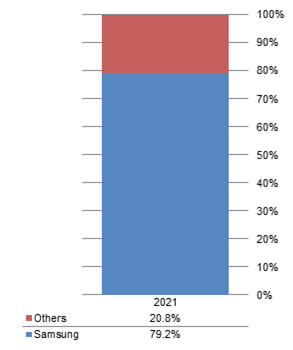

Chart 10: Global foldable smartphone shipment share by top brands, 2021

Introduction

Based on Digitimes Research's statistics and analyses, amid the resurgence of the COVID-19 pandemic and rising concerns over a potential inflation, global smartphone shipments in the second half of 2021 did not see a growth momentum as in the first half and instead declined in both quarters, resulting in overall volumes slipping below 700 million units in the second half of 2021. Shipments in whole-year 2021 amounted to 1.32 billion units, up only 6.1% from a year ago.

The top-6 brands in terms of second-half and whole-year 2021 global smartphone shipments remained the same - Samsung, Apple, Xiaomi, Oppo, Vivo and Transsion. Among them, the four leading China-based brands Xiaomi, Oppo, Vivo and Transsion all enjoyed double-digit on-year growth in their whole-year 2021 shipments.

Based on Digitimes Research's surveys on 5G phone shipments, a total of 530 million units were shipped in 2021 worldwide, surging nearly 80% from the prior year with Apple securing the largest market share of more than 30%. The shipments of foldable phones came short of 10 million units in 2021. Samsung still made the biggest volume of foldable phone shipments, representing close to 80% of the market.

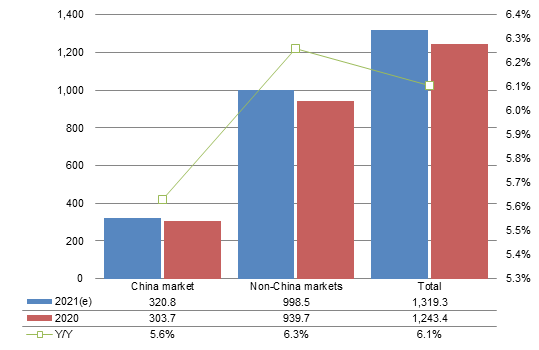

Chart 1: Global smartphone shipments by China and non-China markets, 2020-2021 (m units)

Source: Digitimes Research, December 2021

According to Digitimes Research's statistics, whole-year 2021 global smartphone shipments amounted to nearly 1.32 billion units, up 6.1% from the 2020 level.

Consumer spending remains weak in China so despite a milder COVID-19 influence compared to the rest of the world and 5G phone upgrade demand, smartphone shipments to China only grew 5.8% from a year ago to reach 320 million units, coming short of the level of 370 million units seen in 2019.

Fewer than one billion smartphones were shipped to markets outside of China in 2021, representing an on-year growth of 6.3%, with smartphone demand and shipments falling under the influence of COVID-19 resurgences in second-half 2021.

Shipment breakdown

Quarterly breakdown

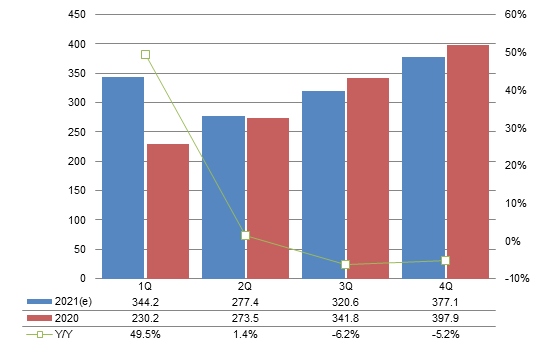

Chart 2: Global smartphone shipments by quarter, 1Q20-4Q21 (m units)

Source: Digitimes Research, December 2021

Breaking down 2021 global smartphone shipments by quarters, first-quarter 2021 shipments topped 340 million units, up nearly 50% from a year ago, showing strong performance in the traditional low season, as the smartphone brands aggressively ramped up shipments in view of the mitigating COVID-19 situation with the prior wave of outbreak waning and vaccinations generating effects.

Going into the second quarter, the outbreak of the Delta variant starting in India and spreading to other regions dampened emerging market demand. Second-quarter 2021 global smartphone shipments therefore only showed flat growth from the level seen in the corresponding period of 2020.

By the third-quarter, the Alpha and Delta variants of the COVID-19 swept across the globe while European and US governments were lowering the amounts of stimulus checks and unemployment benefits or even stopped issuing them so market demand was weakening and thus global smartphone shipments fell 6.2% from the corresponding period a year ago.

Going into fourth-quarter 2021, rapid spread of the Delta and Omicron COVID-19 variants made the situation worse in Europe and the US. On top of that, inflation concerns took a toll on smartphone demand, resulting in global smartphone shipments continuing to suffer from on-year decline, delivering weak performance in the traditional high season.

China and non-China quarterly

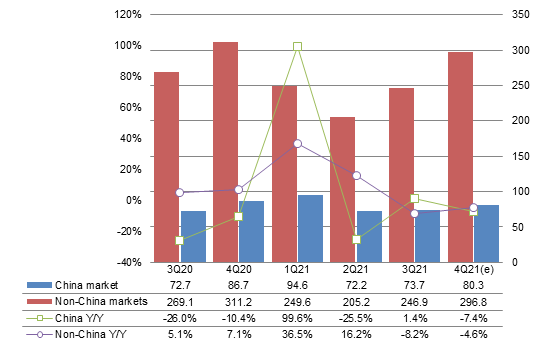

Chart 3: Smartphone shipments in China and non-China markets, 3Q20-4Q21 (m units)

Source: Digitimes Research, December 2021

China's smartphone market showed little improvement in third-quarter 2021 from the second-quarter slump. Third-quarter 2021 smartphone shipments to China exhibited flat growth from the level seen in the corresponding period of 2020 mainly because of the bleak outlook for China's economy and employment market as well as weak consumer demand. The retail channels were still trying to deplete the inventory accumulated in the first half of the year (especially the excess shipments made in the first quarter).

Going into fourth-quarter 2021, thanks to China-based brands' inventory preparation ahead of Singles' Day and Double 12 shopping festivals and brisk sales of Apple's new iPhone 13 in China, smartphone shipments to China had a chance of rebounding to 80 million units, though still coming short of the level seen in the corresponding period of 2020.

As to smartphone shipments to markets outside of China in second-half 2021, the COVID-19 resurgence in the third and fourth quarter in Southeast Asia and Europe not only dampened market demand but also disrupted electronics supply chain operations, resulting in on-year shipment declines for two consecutive quarters.

Top brands

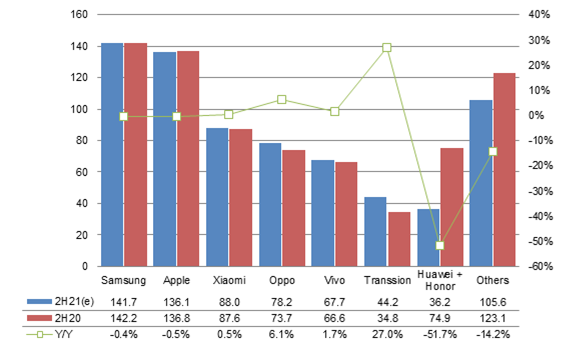

Chart 4: Global shipments by top brands, 2H20, 2H21 (m units)

Source: Digitimes Research, December 2021

According to Digitimes Research's statistics, the top-6 brands in terms of their global smartphone shipments in second-half 2021 were Samsung, Apple, Xiaomi, Oppo, Vivo and Transsion.

The top-5 brands' 2021 shipments showed flat to moderate growth from the 2020 level while Transsion at No. 6 enjoyed an increase of close to 10 million units.

With the US government banning Huawei from accessing some of the key components and Honor having yet gained a foothold after becoming independent, the combined shipments by Huawei and Honor plunged 38.7 million units on year in the second half of 2021.

Shipment share in 2021

Chart 5: Global shipments and share by top brands, 2021 (m units)

Source: Digitimes Research, December 2021

In terms of whole-year 2021 shipments, the four leading China-based brands among the global top-6 vendors enjoyed double-digit growth, benefiting from Huawei losing its presence in the smartphone market and feature phone users upgrading to smartphones in several emerging markets.

Xiaomi, Oppo and Transsion each saw shipments surge more than 30% from the prior year while Vivo also delivered a more than 20% on-year growth in 2021.

Apple and Samsung each enjoyed more than 8% annual growth in shipments in 2021.

The combined shipments of Huawei and Honor showed a larger than 50% decline from Huawei's 2020 shipments.

Global 5G smartphone

Chart 6: Global 5G smartphone shipments, 2020-2021 (m units)

Source: Digitimes Research, December 2021

According to Digitimes Research's statistics, 2021 global 5G phone shipments came close to 530 million units, soaring near 80% from the prior year.

The top-5 brands in terms of 5G phone shipments in 2021 were Apple, Oppo, Vivo, Samsung and Xiaomi, together representing 87% of the market.

As opposed to only shipping 5G phones in the fourth quarter in 2020, Apple marketed 5G-enabled iPhones every quarter in 2021. The full series of the iPhone 13 was built with support of 5G and was enthusiastically embraced by the market, making Apple the largest supplier of 5G phones with a more than 30% market share.

Each of Xiaomi, Samsung, Vivo and Oppo holds a market share somewhere in the range between 11% and 15% in 2021.

Huawei had the highest smartphone shipments in 2020 but the combined market share of Huawei and Honor was only a single-digit percentage as the US government's sanctions restrict its access to some key components.

Chart 7: Global 5G smartphone shipment share by top brands, 2021

Source: Digitimes Research, December 2021

5G smartphone in China and non-China markets

Chart 8: 5G smartphone shipments in China and non-China markets, 2020-2021 (m units)

Source: Digitimes Research, December 2021

Driven by Apple marketing 5G-enabled iPhone 12 and 13 all over the world and Samsung as well as China-based brands making 5G phones available across all price ranges, the shipments of 5G phones to markets outside of China exceeded 270 million units in 2021, doubling the 2020 volumes. The share among the global total also rose to 52.1%, more than half.

As Chinese telecom operators strongly encouraged their subscribers to upgrade to 5G services and China-based smartphone brands scrambled to bring low-cost and mid-range phones to the market, 5G phone shipments to China were already in high gear in 2020 and were still able to further shoot up 50% in 2021 to top 250 million units. The share among the global total however fell to 47.9%.

Foldable smartphone

Chart 9: Global Foldable smartphone shipments, 2020-2021 (m units)

Source: Digitimes Research, December 2021

According to Digitimes Research's study on the shipments of individual brands, 2021 global foldable phone shipments came to 9.4 million units, growing slightly higher than 20% from a year ago.

Samsung shipped close to 80% of the foldable phones in the market. More Galaxy Z Flip phones were shipped than Z Fold phones. The former represented more than 70% of Samsung's foldable phone shipments.

The other 20% were shipped by China-based brands, together delivering no more than two million units.

Global foldable phone shipments came significantly short of the forecast given in early 2021 mainly due to delays in the launch schedules on the part of several smartphone vendors. For example, Oppo and Huawei did not debut Find N and P50 Pocket until the latter half of December. Vivo, Honor, Lenovo (Motorola) and Google plan to launch new foldable phones in 2022.

The tight supply of some components such as high-end smartphone processors also set back Samsung's inventory preparation for new foldable phones to launch in the second half of the year.

Chart 10: Global foldable smartphone shipment share by top brands, 2021

Source: Digitimes Research, December 2021