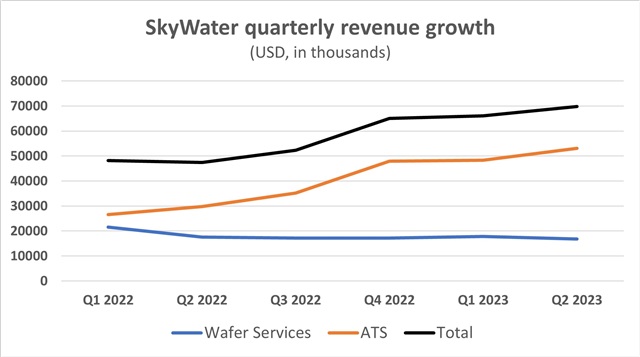

US foundry SkyWater Technology unveiled its second-quarter 2023 earnings on August 7. According to the trusted foundry accredited by the US Department of Defense, on a GAAP basis, revenue increased 47% year-over-year to a record US$69.8 million, while gross margin increased to 23.9%, compared to 4.4% in Q2 2022. The foundry continued to see decreasing net loss, which dropped to US$8.6 million in Q2 2023 compared to US$13 million in Q2 2022.

Together, Advanced Technology Services (ATS) and Wafer Services businesses make up SkyWater's distinct Technology as a Service (TaaS) business model. At the latest earnings call, SkyWater President and CEO Thomas Sonderman noted that the strong Q2 revenue performance exceeds SkyWater's forecast, and the performance to date offers the foundry greater clarity for full-year 2023. Sonderman is confident that the company's long-term annual growth objective of 25% is achievable in 2023, even as leading foundries worldwide see an uncertain and gloomy 2023.

SkyWater also anticipates gross margin acceleration to continue, thanks to the higher revenue volumes that will further absorb fixed costs and position the company in the high-20s and low-30s gross margin level in 2024. The company expects to be nearing its target gross margin objective of 40% by 2025. At the same time, it also aims for a long-term revenue of US$1 billion within a decade.

For Q2, SkyWater's revenue growth was primarily attributed to the restructuring of an existing contract with one of its ATS customers. As development work with the customer entered into new terms, it led to a pull-in of US$3.6 million of revenue that previously was expected to be recognized overtime. "Even absent this pull-in, Q2 revenues were at the upper end of our forecast due to continued strong momentum on mutiple ATS programs," Sonderman pointed out.

As a result of its unique lab-to-fab business model, SkyWater's confidence is largely underpinned by the fact that customer R&D investments continue through this period of overall industry tightening. The foundry sees particularly strong investment in bio-health and advanced computing markets. In the latter sector, SkyWater highlights technologies such as silicon photonics, superconducting film and quantum bits. "Some of these advanced computing programs could exceed multimillions of dollars in revenue for us this year," said Sonderman, who also anticipates that several ATS programs will transition to production in 2024.

Currently, SkyWater has been prioritizing its ATS, leading to flat but consistent wafer services output. However, the foundry expects to grow and scale its wafer sevrices revenue when industrial recovery comes.

As the majority of SkyWater's ATS customers are early-stage and venture-backed companies, Sonderman emphasizes that it is "the very nature of SkyWater's business model." "Our TaaS business model continues to attract innovators with long-tail applications addressing large TAM opportunities," he noted, highlighting the company's business to develop next-gen technologies that are high-value and relatively low volume. "We are not chasing the high-volume, low-mix foundry business from large fabless chip companies. That's the conventional foundry model, not SkyWater's," said Sonderman.

Source: SkyWater, compiled by DIGITIMES