Table 1: Key factors affecting tablet shipments in 4Q15 (Supply)

Table 2: Key factors affecting tablet shipments in 4Q15 (Supply)

Table 3: Key factors affecting tablet shipments in 4Q15 (Demand)

Table 4: Key factors affecting tablet shipments in 1Q16 (Supply)

Table 5: Key factors affecting tablet shipments in 1Q16 (Supply)

Table 6: Key factors affecting tablet shipments in 1Q16 (Demand)

Chart 2: Shipments by product - iPad, non-iPad branded and white-box, 3Q14-1Q16 (m units)

Chart 3: Shipment share by product - iPad, non-iPad branded and white-box, 3Q14-1Q16

Chart 8: Shipments by touchscreen technology, 3Q14-1Q16 (m units)

Chart 9: Shipment share by touchscreen technology, 3Q14-1Q16

Chart 14: Intel tablet shipments and share by OS, 2Q15-1Q16 (m units)

Chart 15: Shipments of detachable notebooks by OS, 2Q14-4Q15 (k units)

Chart 16: Shipment share of detachable notebooks by OS, 2Q14-4Q15

Chart 17: Shipments from Taiwan makers and share of global shipments, 3Q14-1Q16 (m units)

Chart 18: Taiwan tablet shipments by maker, 3Q14-1Q16 (m units)

Introduction

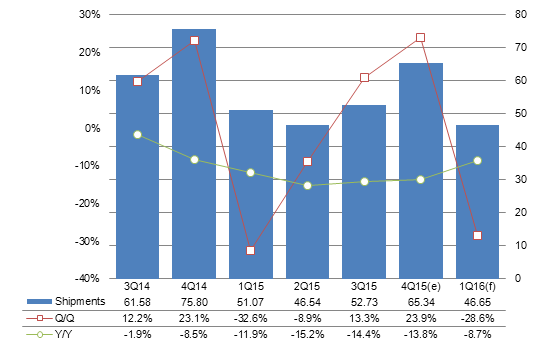

According to Digitimes Research, due to stronger-than-expected demand in the Europe and US markets during the holiday season as well as retail sales channels driving up sales through promotions, shipments volumes from certain US brands were higher than expected during the fourth quarter of 2015, which drove global tablet shipments in the fourth quarter to 65.34 million units, representing 23.9% growth compared to the third quarter, but a 13.8% decline compared to the same period in 2014, though the annual decline was smaller than was seen in the previous two quarters. Although the focus of the market was on the performance of the large-screen-size iPad Pro in the fourth quarter, due to strong promotional pushes in the retail sales channel, shipments of the iPad Air 2 reached 16.1 million units, becoming one of Apple’s primary products in terms of shipments.

White box vendors shipped only 20.3 million products in the fourth quarter, representing a decline of nearly 5% compared to the third quarter. During the busy season, shipments of white box products did not increase but instead decreased due to factors including ultra-low-cost brand-name products penetrating the Europe and US markets, Intel canceling subsidies and vendors turning toward large-screen-size Windows tablets.

Non-Apple brands had the best performance in the tablet market in the fourth quarter, with overall shipments reaching 28.94 million units, representing 6.4% growth compared to the same period in 2014. In the fourth quarter, most of Samsung Electronics’ shipments were low-cost 7-inch products with calling capabilities as well as 9.6-inch models. Due to limited growth in terms of shipment volumes, Samsung trailed behind Apple even more. As in previous years, Amazon significantly increased shipments during the fourth quarter, with its strategy for penetrating into white box product markets using its ultra-low-cost Fire 7 products being successful. This has driven Amazon’s shipment volumes up significantly compared to the same period in 2014. In addition, due to its comprehensive product strategies in the low-end, mid-range, and high-end categories in both the domestic and international markets, Huawei’s shipments exceeded that of Asustek for the first time.

Due to stronger-than-expected iPad and Amazon product shipments, Taiwan-based vendors performed well in the fourth quarter, with shipments reaching 23.32 million units and Foxconn’s share of shipments significantly increasing by nearly 60% due to the iPad Air and iPad Pro. Compal Electronics also benefitted from the iPad mini 2 and the Fire 7 tablet, with the two largest vendors accounting for over 80% of overall shipments.

1Q16 forecast

According to Digitimes Research, due to a slowdown in investment-led growth in China, as well as the impact of a strong dollar on the global economy, the global tablet market (which has entered a mature phase) will experience a significant slowdown in the first quarter of 2016, with most vendors being conservative and cautious toward the market. In the first quarter, global tablet shipments are forecasted to decline by nearly 30% compared to the previous quarter, with only 46.65 million units being shipped, representing an annual decline of 8.6%. However, this would still be an improvement compared to the same period in 2015.

Due to markets in the United States and Europe entering a slow season, as well as the window period prior to the iPad Air 3 becoming available, Apple will experience a steeper decline (with forecasted shipments of only 9.8 million units, which is a historic low and a near 20% decline compared to the same period in 2015) compared to non-Apple brands as well as white box products. Although the previous quarter was considered a busy season, white box products still did not do well. In this quarter, although conversion to 4G is expected to drive sales, a disadvantageous environment as well as competition from low-cost brand-name products will nevertheless result in a decline of over 20% for white box products, with shipments in the first quarter expected to only reach 15.4 million units.

In terms of other brands, Samsung (which is ranked 2nd), whose strategy is shifting towards focusing on notebook products, will experience a sharp decline with respect to new-product shipments in the first quarter compared to previous years. Lenovo, due to its drive to meet its annual goals, is expected to only experience a slight decline in shipments compared to the previous quarter. Amazon, due to strong demand for its ultra-low-cost device models as well as continued market expansion, will break its streak of shipment declines during the first quarters of previous years, and maintain a ranking close behind that of Lenovo. Microsoft, due to strong demand for its Surface Pro 4 products as well as its cooperative efforts with PC vendors from the United States to increase sales in the business-user market, will experience an increase in shipment volumes.

Key factors affecting tablet shipments in 4Q15

Supply side

The performance of most vendors (brands) either met expectations or exceeded expectations in the fourth quarter.

iPad shipments were originally expected to decline significantly due to mainstream 9.7 inch devices not having been updated. However, due to promotional efforts for driving up sales by sales channels such as Best Buy, as well as the effects of users upgrading from iPad 2 devices, shipments of the iPad Air 2 have been driven up significantly. Shipments of the iPad Pro, on the other hand, were close to original expectations.

Shipments of Amazon’s low-cost 7-inch products exceeded expectations, with more than four million units shipped in the fourth quarter.

Due to unclear positioning and a poor price-performance ratio for the large-screen-size mobile phones designed by Lenovo’s Tablet Division, shipment volumes were lower than expected. Tablets that emphasize calling capabilities are mostly 7 inches in size. 7 inch Wi-Fi device models faced strong competition in North America, and shipments are shifting towards 8 inch as well as 10 inch device models.

Note: The more stars, the higher the influence. ↓ indicates negative influence, ↑indicates a positive influence.

Source: Digitimes Research, February 2016

Supply side 2

In the fourth quarter, Intel’s performance in terms of tablets used mainly for communications purposes as well as Cherry Trail processors fell short of expectations.

SoFia 3GR, which has primarily targeted 3G tablets used mainly for communications purposes, was impacted by the price wars between MediaTek and Spreadtrum, resulting in shipment volumes from white-box vendors and brand-name vendors combined falling short of 3 million units.

There was insufficient supply of Cherry Trail products to vendors in Southern China, with sales of new brand-name low-cost 2-in-1 devices remaining slow in the fourth quarter.

The Apple Pencil only supports the iPad Pro. The Apple Pencil’s drawing and writing capabilities as well as certain apps that support the iPad Pro have made the iPad Pro attractive in certain markets. Surface Pen, on the other hand, has improved significantly in terms of response speed, pressure sensitivity, and comfort of writing.

Note: The more stars, the higher the influence. ↓ indicates negative influence, ↑indicates a positive influence.

Source: Digitimes Research, February 2016

Demand side

In the fourth quarter, the demand side was dominated by advantageous factors, including strong demand during the holiday season in North America as well as sales promotions being held by the retail sales channel, which were all conducive toward increasing overall shipments.

A significant increase in sales promotions during the busy season in the United States helped drive demand.

During the Christmas busy season, the price of the iPad Air 2 was reduced by US$100 at Best Buy and the price of Core i5 Surface Pro 3 devices were reduced by US$300. Target, on the other hand, offered iPad Air2 gift cards worth US$150.

Note: The more stars, the higher the influence. ↓ indicates negative influence, ↑indicates a positive influence.

Source: Digitimes Research, February 2016

Key factors affecting tablet shipments in 1Q16

Supply side

In the first quarter, shipment volumes will decline for all brands with the exception of Microsoft, with Apple and Samsung experiencing the steepest declines.

Prior to the introduction to the next version of Apple’s MacBook, Microsoft will continue to drive up sales of its Surface Pro 4, with shipments of the Surface Book also being smoother in the first quarter.

Unlike previous years, during which Amazon’s sales were only strong during the fourth quarter, shipments of its low-cost 7-inch devices will continue to be strong during the first quarter.

Note: The more stars, the higher the influence. ↓ indicates negative influence, ↑indicates a positive influence.

Source: Digitimes Research, February 2016

Supply side 2

In the first quarter, Bay Trail-CR (which is primarily used in 2-in-1 devices) will gradually withdraw from the market, while next-generation Cherry Trail(X5) products still cost more than twice as much (which will be a disadvantageous towards the promotion of such products).

With Wintel leading the way, tablet vendors in the Southern China Region (which were originally a part of the Intel camp) will engage in the development of low-cost notebook products. Therefore, fewer resources will be allocated to the development of Windows tablets.

Note: The more stars, the higher the influence. ↓indicates negative influence, ↑indicates a positive influence.

Source: Digitimes Research, February 2016

Demand side

There will be many negative factors on the demand side during the first quarter.

Slowing growth in China will have a greater impact on demand for brand-name tablets.

A decline in Chinese investment will hurt emerging markets that rely on raw material exports (such as Brazil, Russia, the Middle East, as well as Indonesia) even more. These countries are the primary source of demand for tablets with calling capabilities as well as white box tablets primarily used with Wi-Fi connections.

Note: The more stars, the higher the influence. ↓ indicates negative influence, ↑indicates a positive influence.

Source: Digitimes Research, February 2016

Shipment breakdown

Due to shipment volumes of iPads as well as Amazon products being higher than expected, global tablet computer shipments exceeded 60 million units in the fourth quarter, representing quarterly growth of over 20% as well as an annual decline smaller than that of the previous two quarters.

The primary source of growth was demand during the holiday season in Europe and the United States, as well as sales promotions that were more aggressive than in previous years.

Chart 1: Global tablet shipments, 3Q14-1Q16 (m units)

Source: Digitimes Research, February 2016

1Q16 forecast

With the economic outlook for the global economy looking grim for the first quarter, most vendors will be more conservative compared to previous years. Although declines in shipment volumes will not be as steep as in 2015, a quarterly decline of nearly 30% (and an annual decline of less than 10%) is still expected.

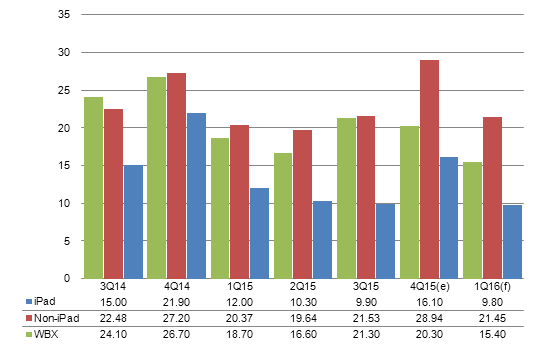

Shipments by product

Performance of iPads and non-Apple brands were better-than-expected, with shipments of non-Apple products increasing slightly compared to the fourth quarter of 2013 and shipment volumes reaching record highs.

Non-Apple vendors successfully rallied against white box vendors, expanding market share in a contracting overall market. The main reasons for this include:

- Brand-name vendors collaborating with the Chinese supply chain and introducing 7 inch tablets with average specs at ultra-low price points designed for use primarily in environments with Wi-Fi connections.

- Smartphone vendors take advantage of brand recognition to aggressively promote tablets used mainly for communications purposes in emerging markets.

Due to competition from brand-name vendors, shipments from white box vendors declined in the fourth quarter compared to the third quarter.

In the fourth quarter, 16.1 million iPads were shipped, exceeding expectations by 2.1 million units, but nevertheless representing a 26.5% decline compared to the same period in 2015.

The better-than-expected performance was primarily due to aggressive promotional efforts for the iPad Air 2.

- 8.6 million 9.7-inch iPads were shipped.

- 5.4 million 7.85-inch iPad minis were shipped.

- 2.1 million 12.85-inch iPad Pros were shipped.

Chart 2: Shipments by product - iPad, non-iPad branded and white-box, 3Q14-1Q16 (m units)

Source: Digitimes Research, February 2016

1Q16 forecast

Due to the effects of the slow season for the Europe and US markets, as well as the window period prior to the introduction of new products, Apple will experience a higher rate of decline compared to other vendors in Q1, with shipment volumes expected to reach historic lows.

Quarterly declines for non-Apple brands will be slightly steeper than the same period last year, but these brands may still experience growth compared to the same period in 2015.

The main reason for this is due to large-screen-size tablet products, low-cost products with calling capabilities, as well as ultra-low-cost 7-inch Wi-Fi products still experiencing strong sales.

White box products will experience the smallest quarterly decline in the first quarter, but they will still experience significant declines of over 15% compared to the same period last year.

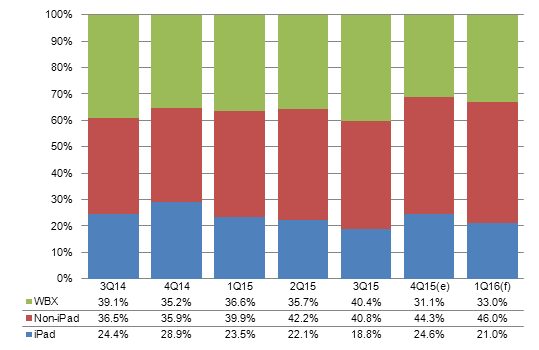

Chart 3: Shipment share by product - iPad, non-iPad branded and white-box, 3Q14-1Q16

Source: Digitimes Research, February 2016

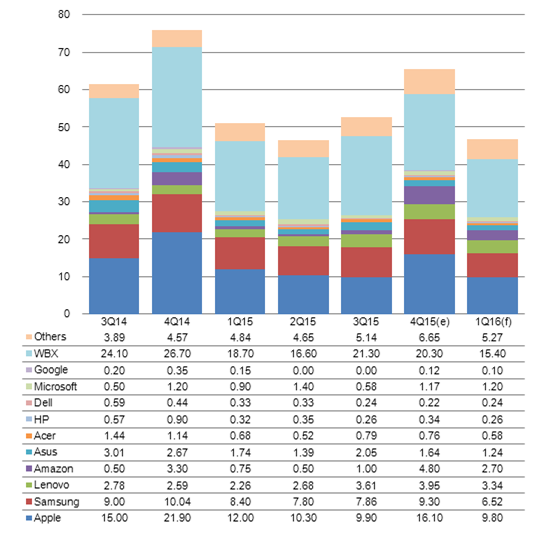

Shipments by vendor

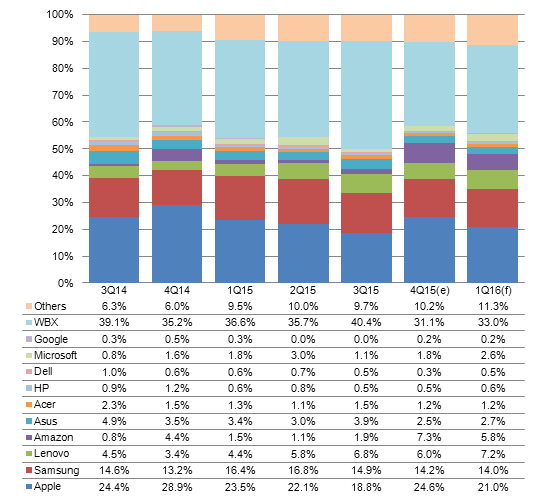

In the fourth quarter, shipment volumes of Apple’s iPad Air 2 were twice as high compared to the previous quarter. In addition, the large-screen-size iPad Pro was introduced. These factors drove Apple’s share of overall tablet shipments up to nearly 25% of overall shipments, making the fourth quarter the quarter of the year in which Apple accounted for the highest share of overall shipments.

Samsung’s defensive strategy of pursuing products similar in screen size to Apple’s products but with low prices was successful, with its share of overall shipments only slightly declining by less than 1 percentage point compared to the previous season.

Amazon began shipping its ultra-low-price 7-inch products during the Christmas busy season in the Europe and US markets, resulting in its shipments (as well as its share of overall shipments) increasing significantly compared to the same period last year and surpassing Lenovo to be ranked third.

In the fourth quarter, Huawei expanded significantly in the China, Southeast Asia, and Europe markets with devices using HiSilicon’s high-end products, Qualcomm’s mid-range products, as well as Spreadtrum’s low-end products, thereby surpassing Asustek in terms of rankings for the first time.

Chart 4: Shipments by vendor, 3Q14-1Q16 (m units)

Note: Google and its brand vendor partners’ jointly developed tablets are included in Google’s shipments

Source: Digitimes Research, February 2016

1Q16 forecast

In previous years, Samsung would take advantage of Apple’s slow seasons (1Q and 2Q) to announce new products and drive up sales. In 2016, however, its strategy is focusing toward notebook products, with only a Windows tablet and an affordable 8-inch product being introduced. This will result in Samsung’s share of overall shipments slightly declining compared to the previous quarter.

In previous years, Amazon’s sales would plummet during the first quarter to a scale of several hundred thousand, resulting in its rankings rapidly dropping.

In 2016, however, due to low-cost device models eating into the market share of white-box products and experiencing strong sales, as well as China’s digital content services becoming more mature, Amazon’s sales figures will remain high, with its ranking expected to be right behind Lenovo (which is ranked third).

Microsoft will ship nearly one million Surface Pro 4 products, resulting in its share of overall shipments in the first quarter experiencing an increase instead of a decline.

Chart 5: Shipment share by vendor, 3Q14-1Q16

Note: Google and its brand vendor partners’ jointly developed tablets are included in Google’s shipments

Source: Digitimes Research, February 2016

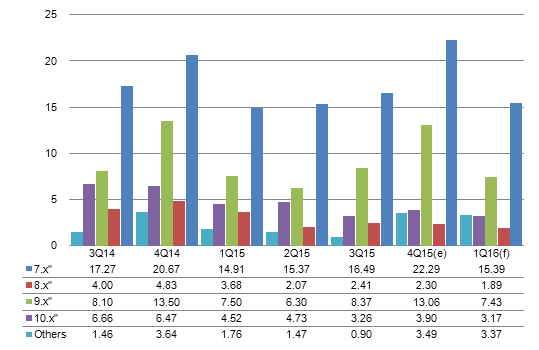

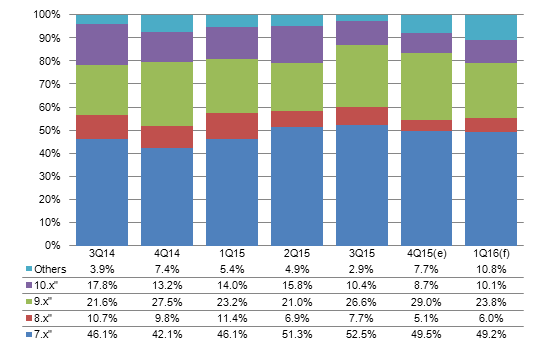

Shipments by panel size

Shipments of 7-inch and 9.x-inch products were better than expected in the fourth quarter and shipment percentages for these product categories (with respect to overall shipments) were higher compared to the same period in 2014.

The reason why 7-inch product shipments were stronger than expected was primarily due to growth in terms of Amazon’s low-cost products as well as communications-oriented products from China vendors.

The reason why 9.x inch product shipments were higher than expected was primarily due to increases in iPad Air 2 shipments as well as Samsung’s low-cost 9.6-inch devices.

Shipments of 10-inch products declined sharply due to the poor performance of 2-in-1 devices from PC brands.

Shipments of 11 in devices exceeded 5% due to significant increases in shipments of iPad Pro and Surface Pro devices.

Chart 6: Shipments by panel size, 3Q14-1Q16 (m units)

Source: Digitimes Research, February 2016

1Q16 forecast

In the first quarter, due to large-screen-size devices (such as the iPad Pro and the Surface series products) maintaining high shipment volumes, the share of 11-inch device shipments with respect to overall tablet shipments will reach a record high.

In the first quarter, the percentage of 7-inch device shipments with respect to overall tablet shipments will reach new highs.

The main reason for this is due to iPad shipments dropping significantly, with Amazon’s 7-inch products experiencing strong sales.

Chart 7: Shipment share by panel size, 3Q14-1Q16

Source: Digitimes Research, February 2016

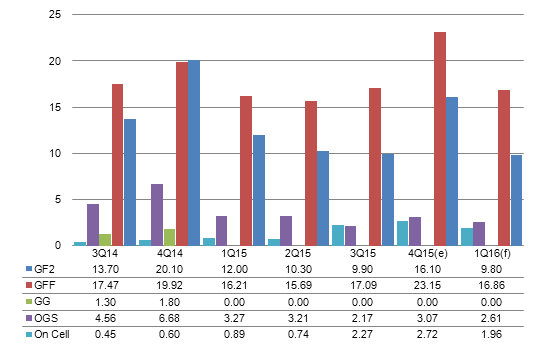

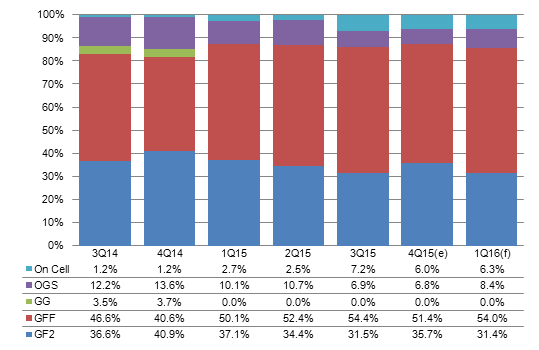

Shipments by touchscreen technology

The percentage of GFF devices is higher than expected, remaining at over 50%.

The main reason for this is due to shipments of Android devices being significantly higher than originally expected.

Chart 8: Shipments by touchscreen technology, 3Q14-1Q16 (m units)

Source: Digitimes Research, February 2016

1Q16 forecast

The percentage of OGS products will increase by 1.6 percentage points compared to the previous quarter due to an increase in high-end large-screen-size Windows devices.

Chart 9: Shipment share by touchscreen technology, 3Q14-1Q16

Source: Digitimes Research, February 2016

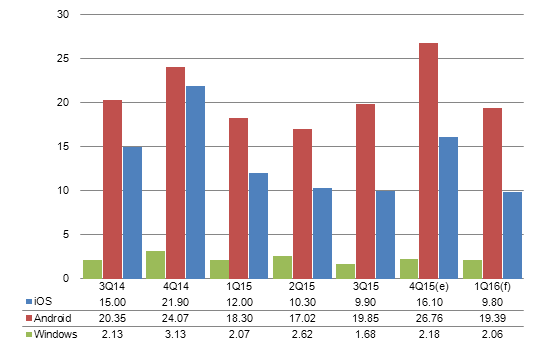

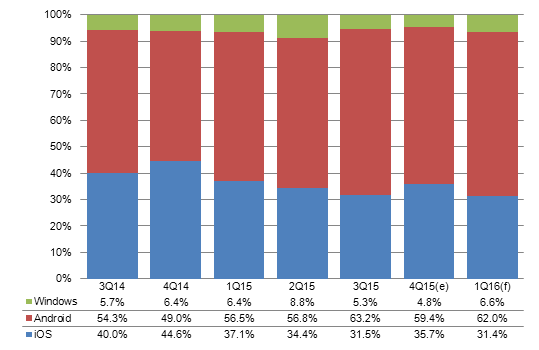

Shipments by OS

In the fourth quarter, iPad shipments increased significantly, driving the percentage of iOS devices back up to over 35%.

The percentage of Windows shipments (with respect to overall shipments) did not meet expectations in terms of growth and actually declined by 0.6 percentage points.

The main reason for this was due to poor performance of 2-in-1 devices from PC brands as well as growth in Android shipments being stronger than expected.

Chart 10: Shipments by OS, 3Q14-1Q16 (m units)

Source: Digitimes Research, February 2016

1Q16 forecast

The percentage of Windows device shipments in the first quarter could increase by 1.8 percentage points.

This is primarily due to the Surface series products experiencing high shipment volumes as well as brand-name 12.x inch PC products beginning to ship during the first quarter.

Chart 11: Shipment share by OS, 3Q14-1Q16

Source: Digitimes Research, February 2016

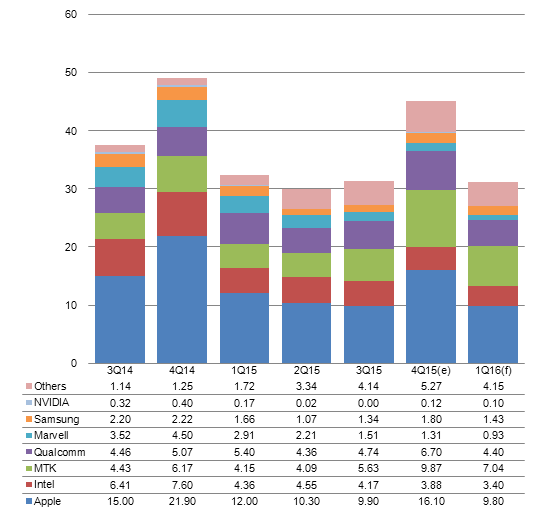

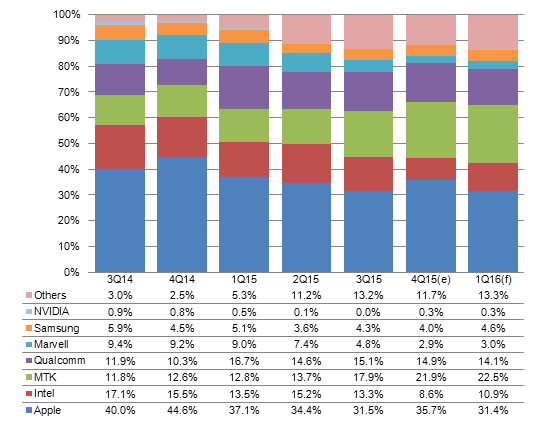

Shipments by AP supplier

Benefitting from Amazon’s 7-inch products continuing to use the MT8127 as well as Chinese smartphone vendors continuing to grow, MediaTek’s shipments surpassed 20% in the fourth quarter.

Due to Asustek’s SoFIA 3GR shipments falling short of expectations as well as poor performance in terms of 2-in-1 devices from PC brands, Intel’s shipments declined significantly.

Chart 12: Shipments by AP supplier, 3Q14-1Q16 (m units)

Source: Digitimes Research, February 2016

1Q16 forecast

During the first quarter, Windows devices will have a stronger performance compared to other types of devices, which will drive the percentage (with respect to overall tablet shipments) of Intel’s x86 processors back up to over 10%.

Low-end devices with calling capabilities benefit from Lenovo’s push to meet its goal for the fiscal year; shipments of Wi-Fi oriented devices remain strong due to Amazon’s products; the percentage of MediaTek products will further increase in the first quarter.

Chart 13: Shipment share by AP supplier, 3Q14-1Q16

Source: Digitimes Research, February 2016

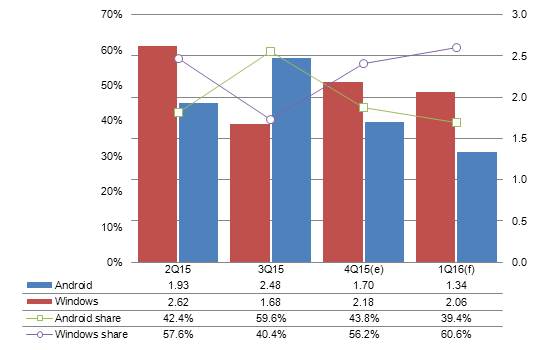

Shipments of Intel-based tablets by OS

The percentage of WOI (Windows on Intel) tablets increased significantly in the fourth quarter.

This is primarily due to shipment volumes of Surface series products as well as Asustek’s SoFIA 3GR devices being lower than expected.

Since Asustek will no longer use Intel solutions for its new Android product development projects in 2016, AOI (Android on Intel) shall slide into obscurity.

Chart 14: Intel tablet shipments and share by OS, 2Q15-1Q16 (m units)

*Note: White box products are not included in the figures.

Source: Digitimes Research, February 2016

1Q16 forecast

The percentage of WOI (Windows on Intel) devices will exceed 60% due to Asustek discontinuing production of Android devices that use the SoFIA processor as well as an increase in brand-name Windows tablets.

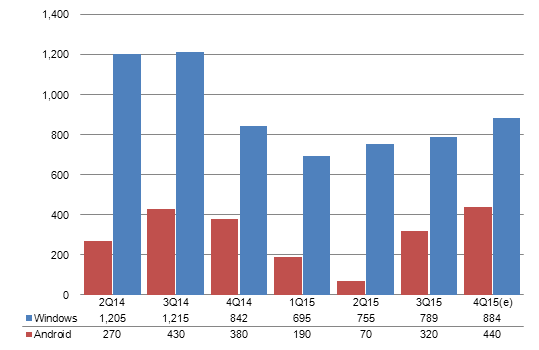

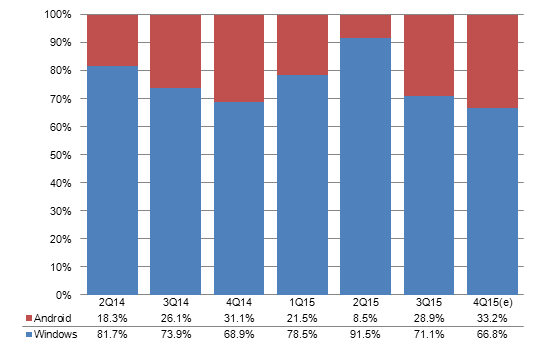

Shipments of detachable notebooks by OS

Shipment volumes of detachable Windows device models that use Cherry Trail X5 processors were lower than expected, with growth in shipments (compared to the previous quarter) being less than 100,000 units.

Chart 15: Shipments of detachable notebooks by OS, 2Q14-4Q15 (k units)

Source: Digitimes Research, February 2016

Chart 16: Shipment share of detachable notebooks by OS, 2Q14-4Q15

Source: Digitimes Research, February 2016

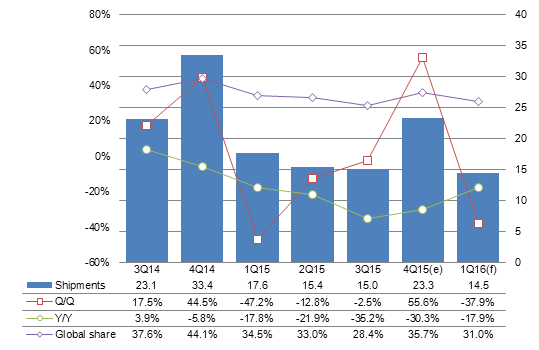

Shipments from Taiwan makers

Demand from the North American market was strong in the fourth quarter, which resulted in US-based brands increasing inventories for the busy season and shipments in the fourth quarter from Taiwan-based vendors exceeding 23 million units.

The percentage of global shipments from Taiwan-based vendors also rose back up to 51.8%, which was the second-highest of the year.

Chart 17: Shipments from Taiwan makers and share of global shipments, 3Q14-1Q16 (m units)

Source: Digitimes Research, February 2016

1Q16 forecast

In the first quarter, sharp declines in iPad shipments will cancel out shipments of Amazon and Windows devices, with shipments from Taiwan vendors reaching record lows.

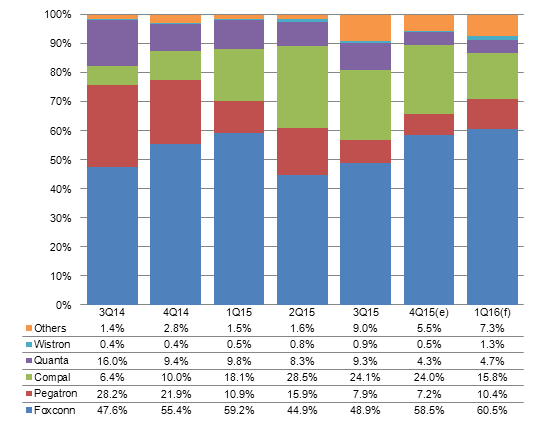

By maker

In the fourth quarter, iPad Air 2 and iPad Air 2 products were provided exclusively by Foxconn, driving its share of shipments up by 9.6 percentage points to 13.65 million units.

Although Compal was not the exclusive provider of Amazon’s 7-inch products, its shipment volumes were slightly higher than those of its competitors. In addition, shipments of the iPad mini 2 have increased during the busy season. These factors have contributed to Compal maintaining a 25% of overall shipments in the fourth quarter, with 5.6 million units shipped.

New Surface device models were the main contributor to Pegatron’s shipments of 1.67 million devices.

Quanta’s share of shipments declined significantly due to a drop in Asustek’s market share and new devices being contract-manufactured by Inventec instead.

Chart 18: Taiwan tablet shipments by maker, 3Q14-1Q16 (m units)

Source: Digitimes Research, February 2016

1Q16 forecast

In the first quarter, the percentage of products coming from Foxconn will increase to over 60%.

Although the impact of the decline in shipments of Apple products will be significant, shipments from other Taiwan-based vendors will decline even more.

The percentage of products from Compal Electronics will sharply decline.

Although overall orders from Amazon will only drop slightly, Compal Electronics’ contract manufacturing market share will be significantly lower than that of China-based contract manufacturing vendors.

Shipments from Pegatron may increase to account for over 10% of shipments from Taiwan-based vendors due to strong sales of Microsoft’s Surface products, even during the slow season.

Chart 19: Taiwan tablet shipment share by maker, 3Q14-1Q16

Source: Digitimes Research, February 2016