As of 2013, the 10 ASEAN nations had a total of over 700 million mobile subscriptions, with the CAGR from 2003-2013 reaching 24%, and the share of the global user base rising from 4.9% to a high of 10.6%. This Digitimes Research Special Report analyzes the various mobile broadband markets in ASEAN and looks at the respective trends in 4G LTE development for those markets.

Abstract

As of 2013, the 10 ASEAN nations had a total of over 700 million mobile subscriptions, with the CAGR from 2003-2013 reaching 24%, and the share of the global user base rising from 4.9% to a high of 10.6%. This Digitimes Research Special Report analyzes the various mobile broadband markets in ASEAN and looks at the respective trends in 4G LTE development for those markets.

Table of contents

Introduction

ASEAN economic overview

Large emerging consumer markets consisting of young consumers

ASEAN achieves economic synergy

Differentiated manpower advantage

Chart 1: ASEAN economies at a glance

Analysis of current ASEAN mobile/fixed-line subscriptions and revenues status

Number of mobile subscribers grows 9-fold over 10 years

Large discrepancies exist between different nations in terms of fixed-line broadband development

Chart 2: ASEAN mobile subscriber data

Chart 3: ASEAN fixed-line broadband subscriber data

Singapore and Malaysia have limited population and their impact on increasing overall mobile service revenues is limited

75% of subscriber ARPU is below US$5

Singapore has high ARPU but lacks growth

Chart 4: ASEAN mobile subscriber ARPU data, 2010-2013

Analysis of mobile/fixed-line industry development in the various ASEAN nations

Growth markets

High-potential markets

Leapfrog markets

Closed markets

Chart 5: ASEAN mobile phones/ mobile broadband penetration rate comparison matrix, 2013

Rugged and scattered territories

Next-generation mobile network technologies undermine fixed-line resources

Penetration rates of smart mobile terminals rapidly increasing

Chart 6: ASEAN fixed line broadband penetration rate comparison matrix, 2013

Observations on the ASEAN mobile industry

Analysis of ASEAN mobile technology and 4G network development

Saturated mobile user markets

Converting from WiMAX to LTE networks

Trends in 4G LTE development

Chart 7: ASEAN markets by technology standards supported, 2013

Good coverage and transmission speeds

Good transmission speed but poor coverage

Poor transmission speeds and poor coverage

Chart 8: Southeast Asia LTE development and coverage matrix, 1Q14

Mobile markets in Singapore

Over-saturated market causing negative growth in revenues

User ARPU on the decline as bonus mobile services are practically useless

Chart 9: Singapore mobile service providers, ARPU, 1Q13-1Q14

Speeding up 3G to 4G migration

Raising capex on networks to speed up LTE upgrades

Developing All over LTE services to increase user data traffic

Chart 10: Singapore mobile service providers transitioning to 4G

Mobile markets in Malaysia

Growth in the mobile user market has reached a saturation point

Entering the explosive growth period for 3G users

Social network services and prices are driving the growth of smartphone penetration rate

Chart 11: Malaysia mobile subscriber data, 2009-2013

LTE post-paid was unpopular and low cost pre-paid plans competed for customers

LTE network coverage is not yet in place

The development positioning of LTE/WiMAX is unclear

Chart 12: Malaysia wireless broadband user data, 2013

Mobile markets in the Philippines

Developing market

SMS is an important source of revenues

Next-generation mobile broadband subscribers have become the highlight of revenues growth

Chart 13: Philippines mobile subscriber data, 2009-2013

Lack of significant speed boost

Low LTE network coverage

Chart 14: PLDT transition to next generation network facing bottlenecks

Mobile markets in Indonesia

The first phase of reform (1989-1999)

The second phase of reform (1999-2009)

Chart 15: Indonesia mobile subscriber data, 2009-2013

Profits remain high

Telecommunications market shows lack of competitiveness

Chart 16: Indonesia telco operators not riding the wave to LTE

Estimates of mobile and 3G/4G subscriptions in ASEAN

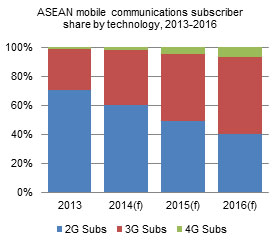

Negative growth of ASEAN mobile subscriptions in 2016

3G user numbers enter market take-off phase 4G users could reach 50 million in 2016

Chart 17: ASEAN mobile users, 2012-2016

Chart 18: ASEAN subscribers by technology, 2013-2016

Observations on the ASEAN fixed-line industry

Development of the ASEAN fixed-line broadband market

Vietnam

Thailand

Singapore

The Philippines

Indonesia

Malaysia

Brunei

Cambodia

Table 1: ASEAN broadband policies by country, 2008- 2014

Rapid growth in number of ASEAN fixed-line broadband subscriptions

Fixed-line broadband penetration rates grow exponentially

Chart 19: ASEAN and global fixed broadband subscribers, 2003-2013 (million)

Chart 20: ASEAN fixed broadband household penetration rate by country, 2003-2013 (million)

SWOT analysis of fixed-line broadband development in ASEAN

Priority in increasing penetration rate of fixed-line broadband subscriptions

Diverse integrated heterogeneous broadband networks

Chart 21: ASEAN broadband policy goals by country, compared with 2013 actual growth

Policy subsidies and education

Develop differentiated value-added services for fixed-line broadband

Create healthy fixed-line broadband market completion

Chart 22: Relationship between fixed-line broadband outlays and gross national income, by country, 2013

Charges unfavorable for IPTV user development

Low bandwidth affecting user experience

Lack of differentiation services

Chart 23: IPTV deployment data among broadband users by region, 2013

Strengths

Weaknesses

Opportunities

Threats

Chart 24: SWOT analysis for broadband development in the ASEAN region