The global LED industry was less buoyant in 2011 than in 2010, and there has been a corresponding slowdown in the deployment of new MOCVD machines. Digitimes Research projects that global MOCVD shipments for 2011 will reach 690 units, a 14% drop on the 800-unit figure for 2010.

Nevertheless, China will account for a greater share of this demand than any other region in 2011 with some 57% of shipments. The next three regions by MOCVD demand - Taiwan, Japan and South Korea - will each account for less than 10% of global demand. It is therefore clear that the importance of the China LED industry on the global stage is increasing.

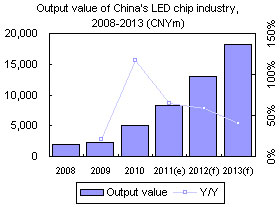

While China is scaling back its subsidy policies for MOCVD units, the country's enormous MOCVD capacity is likely to drive growth in LED chip output value in the coming years. Digitimes Research projects that LED chip output value in China will reach CNY13.0b (US$2.05b) in 2012 and CNY18.25b in 2013, representing tenfold growth over the 2008 figure.

Thanks to its MOCVD subsidy programs, not only is China the global center of MOCVD equipment demand, but the country's LED industry has also gradually improved its global standing. However, the country's LED chip manufacturers remain an extremely mixed bag in terms of competitiveness. The 12th FYP aims to remedy this situation by consolidating this disparate range of companies into a handful of serious competitors, in order to put the China industry on a par with those of Europe, North America and Japan, which each boast two or three major manufacturers.

For the reasons outlined above, in particular smaller players' plans to sell off MOCVD capacity to larger manufacturers, Digitimes Research projects that the China LED chip industry will become increasingly concentrated in the hands of the big six manufacturers: Sanan, Electech, Tsinghua Tongfang, Silan Azure, Epilight and Changelight. More and more smaller manufacturers in China are withdrawing from the LED chip sector altogether and selling off their MOCVD capacity to larger, more stable firm. Digitimes Research therefore projects that the level of concentration in the China LED chip industry will continue to increase, rising to 57% by 2013.

Chart 1: Global shipments of MOCVD units for LEDs, 2006 -2011

Chart 2: Distribution of MOCVD units by geographic region, 2011

Distribution of MOCVD capacity for China's LED manufacturers

Table 1: Major China-based LED chip manufacturers' MOCVD unit delivery status in 2011

Chart 3: Output value of China's LED chip industry, 2008-2013 (CNYm)

Chart 4: LED chips as a percentage of overall LED industry output value in China, 2008-2013 (CNYm)

Table 2: Government policies and targets for the LED industry in China

Chart 5: Distribution of revenues and operating profits for China's major LED chip makers, 2010-2011

Chart 7: Total number of MOCVD units for China's major LED chip makers, 2010-2011

Table 3: Comparison of the technical capabilities of China's major LED chip makers

Table 4: Industry presence for China's major LED chip manufacturers

Output value forecasts and concentration analysis for China's major LED chip makers

Chart 8: Total output value for China's big six LED chip makers, 2008-2013 (CNYm)

Chart 9: Big six LED chip manufacturers' share of the China LED chip industry, 2008-2013

Chart 17: Global LED chip output value by region and Sanan's share of China LED chip output value

Chart 18: Bottlenecks in Sanan's development in the LED sector

Chart 22: Electech's overall margins and LED business margins, 2009-1H11 (CNYm)

Chart 23: Government subsidies received by Electech in 1H11 (CNYm)

Chart 24: Electech's MOCVD equipment orders and delivery status

Chart 25: Electech's LED-related fundraising activities, 1H11

Chart 28: Origin of the Electech Group's LED-related technologies

Chart 32: Funding and technology involved in Phase I of Tongfang's Nantong investment

Chart 33: Breakdown of revenues from Tongfang's LED business

Chart 38: Tongfang capacity for LED TV and lighting products

Chart 39: Tongfang's development of LED technology, 2008-2011

Table 5: The business of Silan Azure's package subsidiary Multi-Color

Chart 45: Breakdown of Multicolor's LED package product types

Chart 48: Epilight's revenues and net profits, 2007-2010 (CNYm)

Chart 49: Epilight's production bases and capacity distribution

Chart 52: Changelight revenues and operating profits, 3Q10-2Q11 (CNYm)

Chart 54: Government subsides received by Changelight, 2009-2010

Chart 55: Changelight's MOCVD unit orders and delivery status up to 2012