Introduction

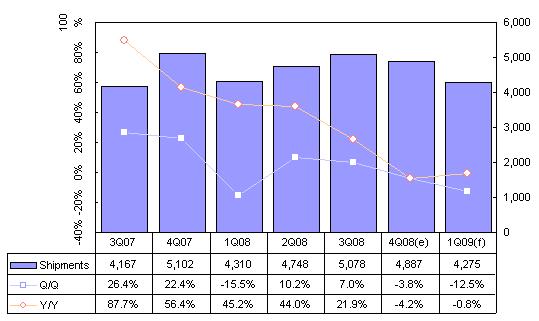

- Taiwan shipped 4.89 million LCD TVs in the fourth quarter of 2008, down 3.8% sequentially and down 4.2% from the same period one year earlier.

- LCD TV shipments will drop 12.5% in the first quarter of 2009, with on-year growth staying flat at -0.8%.

- Taiwan shipped 19.02 million LCD TVs in 2008, representing growth of 22.5% from 2007, compared to global growth of 28%.

- For 2009, Taiwan shipments are expected to increase 21.4% to reach 23.1 million units. Global shipment growth will increase 19.2% to reach 115 million units.

- Taiwan had a global share of 19.7% in 2008 and that is forecast to increase to 20.1% in 2009.

NOTE: Unless otherwise indicated, all figures and tables in this report refer to output from Taiwan makers

Chart 1: Taiwan LCD TV shipments, 3Q07-1Q09 (k units)

Source: Digitimes Research, January 2009

Industry watch

- Taiwan LCD TV makers experienced sequential and on-year shipment declines in the fourth quarter of 2008, reflecting a weak year-end holiday season amid the worsening global economy.

- Rush orders, which are usually seen during the last quarter of a year, hardly came in the fourth quarter of 2008.

- Inventory issues and the depreciation of the Korean currency continued to drag down quotes for TV-use panels. Quotes for 32-, 37- and 42-inch TV panels went down 23%, 17% and 15%, respectively, in the fourth quarter of 2008.

- Korean makers were able to offer OEM quotes of US$135-140 for a 32-inch in the fourth quarter, compared to US$150-160 quoted by Taiwan competitors. The Korean suppliers' competitive pricing was enabled by the country's weak currency, which had depreciated over 40% against the US dollar during the latter half of 2008.

- The falling panel prices resulted in lower LCD TV prices. The ASPs of 32-, 37- and 42-inch models continued to slide in the fourth quarter of 2008. The ASP of mainstream 32-inch LCD TVs went down 36% on year, compared to an annual drop of 15% seen in the same period of 2007.

Source: Digitimes Research, March 2009

- Toshiba plans to more than double its LCD TV outsourcing to Taiwan in 2009. The Japanese vendor is expected to place orders of five million LCD TVs with Taiwan suppliers this year, compared to two million units last year.

- The rising orders from Toshiba will allow Taiwan's global share to climb 0.4 percentage points this year.

- Orders from Top-6 vendors (Samsung, Sony, Sharp, LGE, Philips and Toshiba) are expected to account for 34.3% of Taiwan's overall ODM/ OEM shipments in 2009, up 4.9 percentage points. Except for Toshiba, Taiwan shipments to the other top-tier vendors will remain unchanged compared to 2008.

| Table 2: ODM/OEM shipments to Top-6 and non Top-6 brands | |||

|

| 2008 | 2009(e) | Y/Y |

| Top-6 brands | 29.4% | 34.3% | +/- 4.9pp |

| Non Top-6 brands | 70.6% | 65.7% | |

Source: Digitimes Research, March 2009

- In 2008, first-tier LCD TV brands reached a 76% market share, and their dominance is expected to continue growing. This may mean good news for Taiwan's makers, who may receive more outsourcing from the top-tier brands.

- Although Toshiba's increased outsourcing may drive up the ratio of Taiwan's ODM/OEM shipments to first-tier brands in 2009, only first-tier makers TPV, Amtran, Proview, Compal and Wistron will be the major beneficiaries of the Japan vendor's orders. In 2008, shipments from Taiwan's non-Top-5 LCD TV makers totaled less than 700,000 units, compared to 13.96 million units shipped by the Top-5 players.

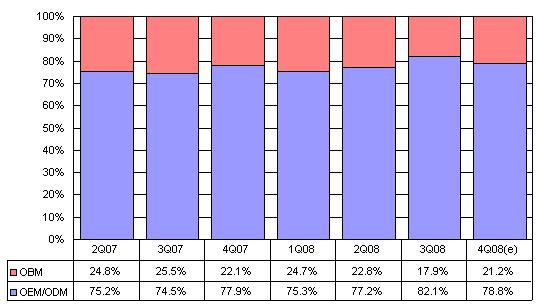

- As for Taiwan's own-brand shipments, the share of OBM went down two percentage points to 21.6% in 2008, as Kolin's gradually phased out it’s the LCD TV production amid a financial crisis inflicted on it by its partnership with the now bankrupt Syntax-Brillian.

- The Top-5 makers will ship around two million LCD TVs in 2009, further expanding their combined share of Taiwan's overall shipments.

- TPV is expected to secure orders for more than 1.2 million units from its Top-3 customers this year. The orders will allow the number-one supplier to enjoy a 48% growth in shipments. Second-place Amtran will have lower growth in shipments this year, as sales of Vizio LCD TVs may be affected by top-tier brands' price cuts.

- Among the first-tier makers, only Proview will suffer a shipment drop in 2009 as the company is restructuring its customer base. The third-place supplier has recently shifted its client focus from second-tier brands to North American channel, and it will also seek to work with channel in other regions.

- Compal entered the Top-5 ranking in 2008 from eighth place in 2007. Being the major beneficiary of Toshiba's increased orders, Compal will see its 2009 shipments rise dramatically.

- Wistron, which remained in fifth place in 2008, will record the second-largest growth among the Top-5 makers in 2009. The company's LCD TV business has grown progressively over the last three years, thanks to contribution from Sony and Westinghouse.

Source: Digitimes Research, March 2009

Shipment breakdown

Business model: OBM, OEM and ODM

Chart 2: Taiwan LCD TV shipments by business model, 2Q07-4Q08

Source: Digitimes Research, January 2009

- The rise in the OBM (own-brand made) share in the fourth quarter was due to Amtran Technology's own-brand shipment growth. Amtran's fourth-quarter own-brand shipments (Vizio brand) were about 150,000 units more than the volume in the previous quarter, despite the economic downturn.

Geographic markets

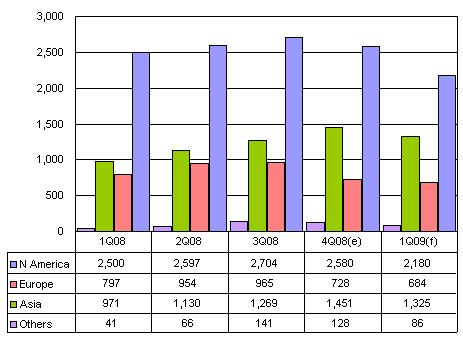

Chart 3: Taiwan LCD TV shipments by region, 1Q08-1Q09 (k units)

Source: Digitimes Research, January 2009

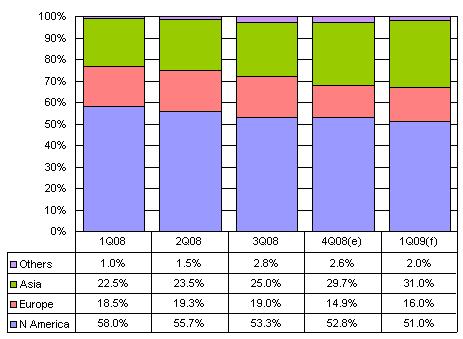

Chart 4: Taiwan LCD TV shipment share by region, 1Q08-1Q09

Source: Digitimes Research, January 2009

- North America, which accounts for more than 50% of Taiwan's LCD TV shipments, is the chief market for Taiwan's top-three makers, TPV Technology, Proview and Amtran.

- Compal Electronics and Wistron, positioned as the fourth and fifth Taiwan ranked makers, ship mostly to Asia, which accounts for more than 60% of the two makers' combined shipments.

- The share of shipments going to Asia continued to grow in the fourth quarter of 2008 because of demand from emerging markets.

- In the first quarter, the shares of Europe and Asia will rise because of Toshiba's increased shipments to the two regions. (The Asia orders will go to Compal while the Europe orders will go to TPV)

Screen size

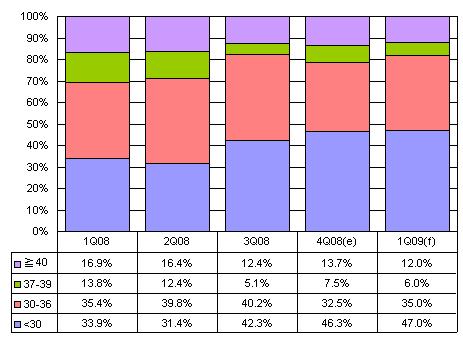

Chart 5: Taiwan LCD TV shipment proportion by screen size, 1Q08-1Q09

Source: Digitimes Research, January 2009

- Orders for 29-inch and below LCD TVs increased in the fourth quarter, as first-tier brands outsourced more low-cost and low-margin products in order to stay competitive during the economic slowdown.

- Thanks to strong sales of Amtran-made Vizio LCD TVs, the proportion of the 40-inch or above segment grew slightly.

- In the first quarter, the 32-inch segment's share will grow on shipments to Toshiba. The share of the 40-inch and above segment will fall back to the third-quarter level, as Vizio's holiday promotional sales have come to an end.

Shipment by maker tier

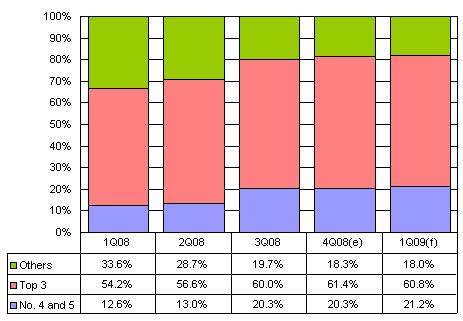

Chart 6: Taiwan LCD TV shipment by maker tier, 1Q08-1Q09

Note: Top-five makers in 4Q08 were TPV, Amtran, Proview, Compal and Wistron

Source: Digitimes Research, January 2009

- Amtran climbed to second place in the fourth quarter, surpassing Proview, which was number one in the third quarter. Amtran's impressive shipments contributed to the rise in the shipment proportion of the Top-three markers.

- Compal's made share gains in the fourth quarter. The maker will manage to maintain its number four spot in the first quarter of 2009, thanks to orders from Toshiba.

- Suppliers like TPV and Proview are expected to benefit from a China government-backed stimulus plan (from end-2008 to January 2013) meant to increase electronics products' penetration in the country's rural areas.

Outlook till 2011

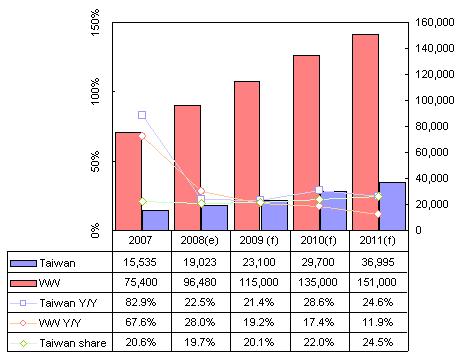

Chart 7: Taiwan LCD TV shipment forecast, 2007-2011 ( k units)

Source: Digitimes Research, January 2009

- Taiwan makers mostly ship to second-tier vendors and North American clients, both of which were more susceptible to the economic downturn. Taiwan's share slid to 19.7% in 2008. But its share will rise in 2009 because of orders from Toshiba.

- Demand from emerging markets is expected to grow sharply, providing opportunity of shipment growth for Taiwan makers through 2011.