Introduction

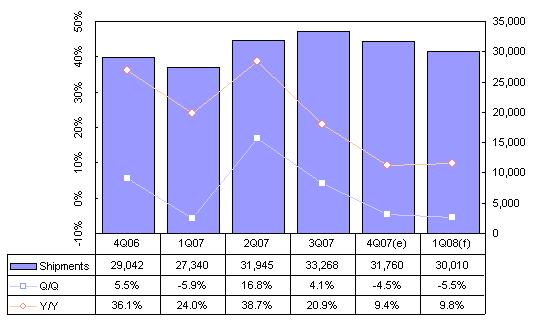

Taiwan shipped 31.8 million LCD monitors in the fourth quarter of 2007, down 4.5% sequentially but up 9.4% from the same period one year earlier.

LCD monitor shipments will fall 5.5% in the first quarter of 2008, but will be up almost 10% from the same period in 2007.

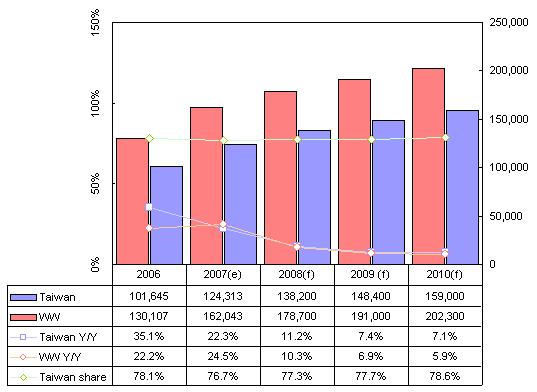

Taiwan shipped 124 million LCD monitors in 2007, up 22% from 2006, while the global growth rate was 25% to reach 162 million units. Taiwan will ship 138 million LCD monitors in 2008, representing growth of 11.2% from 2007 and outpacing the global growth rate of 10.3%.

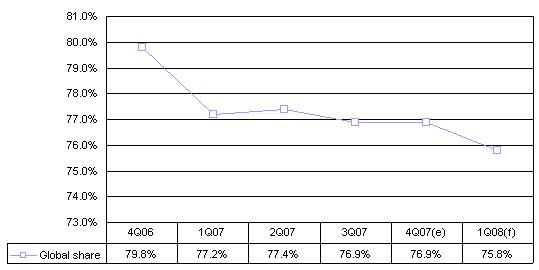

Taiwan accounted for 76.7% of the global LCD monitors market in 2007 and the share is forecast to increase to 77.3% in 2008.

4Q review and forecast

Shipments

Decreasing shipments among Taiwan makers in the fourth quarter of 2007 corresponded closely to the prediction Digitimes Research made in the previous quarter. Lite-On Technology was the only Top-5 maker to increase its shipments more than 4% in the fourth quarter of 2007.

Overall, demand was not strong for Taiwan's LCD monitor makers during the fourth quarter due to the growing trend of notebooks replacing desktop PCs.

Leading LCD monitor maker TPV Technology was not able to grab customers and increase its shipments in the fourth quarter, despite Chi Mei Optoelectronics (CMO) discontinuing its LCD monitor business, which was expected to boost TPV's sales. The two companies had entered into a strategic partnership at the end of the third quarter.

Another reason shipment growth was constrained was that Taiwan makers lacked panel supply during the October hot season. In addition, during the quarter, Innolux Display focused more on small- to medium-size products than on LCD monitor products.

For the first quarter of 2008, despite China's heavy snowfall in late January causing Taiwan's LCD monitor shipments in February to greatly drop, shipments in March have gradually recovered, which will reduce the impact on first-quarter shipments.

In addition, although a February 3 fire at the Lite-On Technology Dongguan factory has led other rivals such as Innolux Display, Qisda, Proview, and TPV Technology to win more LCD monitor orders, it requires a few weeks for customers to shift their orders, so Taiwan's first-quarter LCD monitor shipments are still expected be only slightly affected.

Chart 1: LCD monitor shipments, 4Q06-1Q08 (k units)

Source: Digitimes Research, January 2008

ASP

Although the overall ASP fell 2% in the fourth quarter, shipments of larger-sized monitors dropped while shipments in the 15-inch and 17-inch segments were up, meaning that prices in the market were not dropping

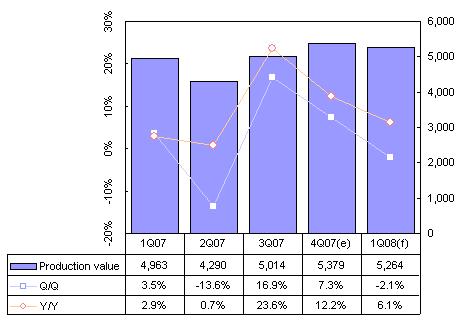

Chart 2: Taiwan LCD monitor production value, 4Q06-4Q07 (US$m)

Source: Digitimes Research, January 2008

Market share

The Top-5 makers in the fourth quarter were TPV Technology, Innolux Display, Lite-On, Qisda and Proview, based on shipment totals. Lite-On was the only maker with more than 4% sequential growth during the quarter.

Despite Chi Mei Optoelectronics (CMO) discontinuing its LCD monitor business, TPV Technology was not able to grab customers and increase its shipments in the fourth quarter. Taiwan LCD monitor shipment volumes in December were also lower than that of Korea-based LCD monitor makers such as Samsung and LG Electronics.

In addition, some makers faced inventory issues among their customers in the fourth quarter, which affected their shipments after November., while major Taiwan LCD monitor maker Innolux Display, which produced 35-40% of its own panels, focused more on small-and-medium size applications in the fourth quarter.

Overall, Taiwan's share of global LCD monitor shipment fell to 75.8%, its lowest level since 2006.

Chart 3: Worldwide market share, 3Q06-4Q07

Source: Digitimes Research, January 2008

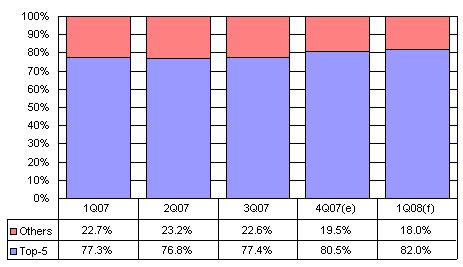

Shipment concentration

The Top-5 Taiwan makers – TPV, Innolux, Lite-On, Qisda and Proview – have been steadily increasing their share of overall shipments, with their overall share reaching just under 80% for the full year 2007.

Although the Top-5 saw strong shipment growth in the third quarter of 2007 – Innolux, Qisda and Proview all increased their respective shipments by more than 9% – their shipment growth was much lower in the fourth quarter, except for Lite-on.

CMO was ranked among the Top-7 makers early in 2007, but in the fourth quarter of the year, the company phased out its LCD monitor business, which contributed to the Top-5 makers increasing their share to 82%, from 80.5% in the third quarter.

The Top-2 Taiwan LCD monitor makers, TPV and Innolux Display will continue to boost their respective shipments in 2008, which will be a major threat to Taiwan second-tire LCD monitor makers. With TPV and Innolux enjoying the profits of an increased production scale, it is unlikely that the concentration rate will reverse direction in the future.

Chart 4: Top-5 makers' share of Taiwan LCD monitor shipments, 4Q06-4Q07

Source: Digitimes Research, January 2008

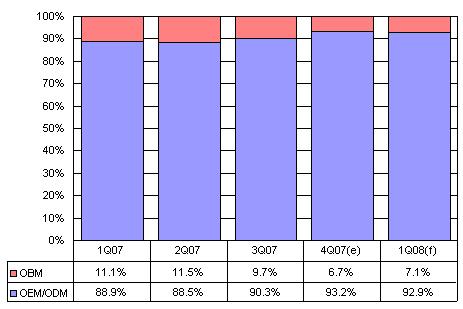

OBM, OEM/ODM breakdown

Most Taiwan-based LCD monitor makers focus on OEM/ODM business, but TPV Technology and Proview are trying to increase their own-brand LCD monitor business.

In addition, with Dell and Hewlett Packard (HP) realizing demand for LCD monitor was sluggish, they reduced their OEM/ODM orders to TPV and Proview. Therefore, Taiwan's own-brand shipment share increased to 7.1%, up 0.3% sequentially,

However, for the year, Taiwan's OEM/ODM share increased to 91.2%, the highest ever, while the OBM share fell from 11.8% in 2006 to 8.8% in 2007. The main reason was that Chi Mei withdrew from the LCD monitor manufacturing business in the latter half of 2007.

Chart 5: Taiwan LCD monitor share by production mode, 4Q06-4Q07

Source: Digitimes Research, January 2008

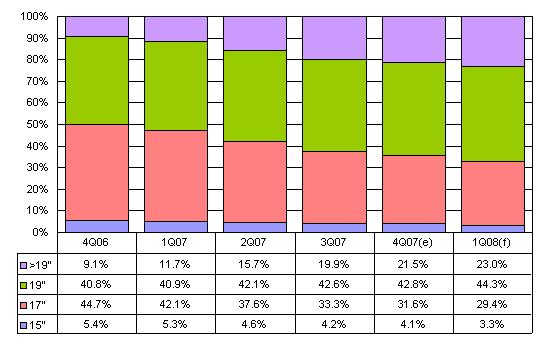

Screen size

While many Vista OS desktop PCs adopt larger than 19-inch LCD monitors – dropping demand for 17-inch panels and eroding the share of the 17-inch LCD monitor segment – TPV and Lite-On are still manufacturing 17-inch LCD monitors for leading vendors, while Innolux Display is Taiwan's biggest OEM maker for 17-inch LCD monitors. So, the segment still accounted for 30% of total LCD monitor shipments in the fourth quarter.

In the 19-inch segment, traditional (4:3 screen ratio) LCD monitors accounted for only 16.2% of total monitor shipments, with TPV and Lite-On being the main suppliers. In the 19-inch segment, the shipment share of widescreen monitor surpassed that for traditional (4:3 screen ratio) models in the fourth quarter, with widescreen models accounting for 64% of the 19-inch segment.

The worldwide Top-2 LCD monitor panel makers, Samsung Electronics and AU Optronics (AUO) focus more on 19-inch widescreen LCD monitor shipments and have reduced their share of traditional 19-inch panel production.

Shipments of 20-inch and larger LCD monitors were up 12.5% in the fourth quarter, after rising 48% and 26% in the previous two quarter. The segment should see continued growth in the first quarter of 2008, with shipments expected to rise 2%, which would make it the only segment seeing growth in the quarter.

In addition to demand from new PCs using the Vista OS, larger sized screens are popular with industries such as financial institutions. The 22-inch segment remains the mainstream for these large monitors. In the fourth-quarter, Taiwan's shipment share of 22-inch widescreen LCD monitor was 13.8%, up 11 percentage points from the same period one year earlier. Due to the segment being the most economical cut for 5.5G, 6G, and 7.5G LCD panel plants, LCD monitor makers were active in developing the segment.

However, the market for extremely large LCD monitors remains niche, with the larger than 23-inch widescreen segments accounting for only 1.2% of total shipments in the fourth quarter.

Chart 6: LCD monitor share by screen size, 4Q06-1Q08

Source: Digitimes Research, January 2008

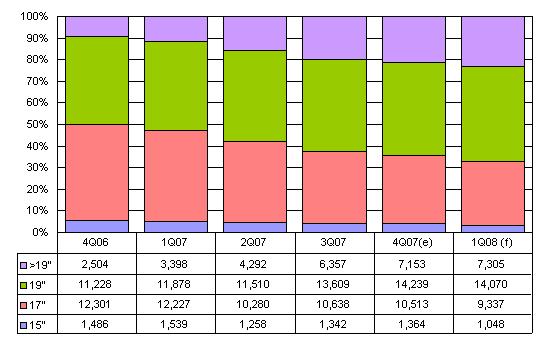

Chart 7: LCD monitor shipments by screen size, 4Q06-1Q08

Source: Digitimes Research, January 2008

Industry watch

Short-term effects of Lite-On plant fire

Due to the February 3 fire at the Lite-On Dongguan factory, international LCD monitor makers such as Dell and Lenovo China were forced to shift their OEM orders to TPV, Innolux and Qisda.

The ranking of Taiwan makers in terms of LCD monitor shipments has not fluctuated much for the past five quarters and Lite-On and Qisda have been jockeying for position since the first quarter of 2007. However, due to the February 3 fire, the company is expected to see its LCD monitor shipments greatly reduced in the first quarter, and the company will fall behind Qisda and become the Number 5 maker.

Proview is unlikely to benefit from Lite-On's decreased shipments, as clients of the two companies do not overlap, so Proview's ranking is expected to remain unchanged.

Although Lite-On LCD monitor OEM orders will shift to other Taiwan markers, these orders are expected to flow back to the company in the second and third quarter of 2008.

2008 and beyond

Taiwan shipped 124 million LCD monitors in 2007, accounting for 76.7% of the global market. Taiwan's global share should increase to 77.3% in 2008, as more Korean makers abandon the low-profit smaller sized segments.

With the economic scale and low-cost advantage, TPV Technology and Innolux Display are expected to take the lead in the growth of LCD monitor shipments from 2008 to 2010.

Chi Mei Optoelectronics (CMO) and TPV Technology formed a strategic partnership in the TFT LCD production chain in the latter half of 2007. The alliance provides CMO a stable outlet for its panel output and TPV a sustainable long-term supply of key components.

Innolux is active in seeking OEM orders from Korea-based makers and the company is looking to increase its capacity by adding one more 6G plant.

Thanks to solid panel supply from AU Optronics (AUO), Qisda will increase the ability of receiving more LCD monitor orders.

As the majority of US-branded LCD monitor vendors release OEM order to Taiwan makers, the key to increasing Taiwan LCD monitor shipments will be to win OEM orders from Korea-based LCD monitor makers such as Samsung Electronics and LG Electronics. Although Korean makers are not expected to release a large number of OEM orders to Taiwan, the situation will change in 2008 as they consider maintaining their profits.

The growth rate of the global LCD monitor industry is unlikely to exceed 10% in 2008, as LCD monitor demand comes from the desktop PC segment mostly, and the annual growth rate of desktop PC shipments will be lower than 5% from 2008 to 2010.

Due to limited growth in demand, leading panel makers have taken a conservative estimate for LCD monitor panel shipments to LCD monitor makers. Panel makers estimate that LCD monitor panel shipments to the Top-7 leading LCD monitor suppliers will total 176 million units, up 9.3% in 2007.

Chart 8: Global LCD monitor shipments, 2006-2010 (k units)

Source: Digitimes Research, January 2008

NOTE: Unless otherwise indicated, figures and tables refer to output from Taiwan makers.